Just a quick post to let everyone know that Thomas and me are attending Nordic Game up North in Malmo this week. Thomas will be speaking on Thursday 24th May at 2pm in a panel about game financing. Hope to see many of you there!

I was asked recently by a friend if I had some numbers about the tablet market in Europe, so I thought I could as well write a blog post about it.

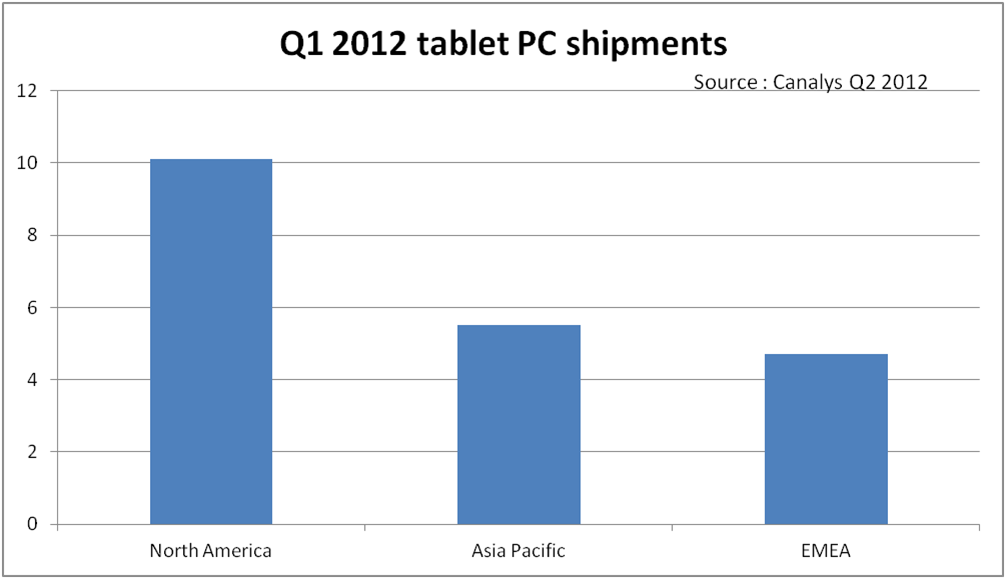

To make it short : Yes, the tablet market is growing in Europe. According to market research institute Canalys, shipments are up 180% yoy to 4.7 million in EMEA. Nonetheless, the growth has been much slower than in the US and Asia Pacific. The research points difficult economic conditions in Europe (according to Gartner, PC shipments declined too), and the lack of content compared to the US (less localised services, such as Netflix & Hulu, and less local(ised) content on Apple, Google and Amazon).

I’ve made a quick chart to summarise the shipments :

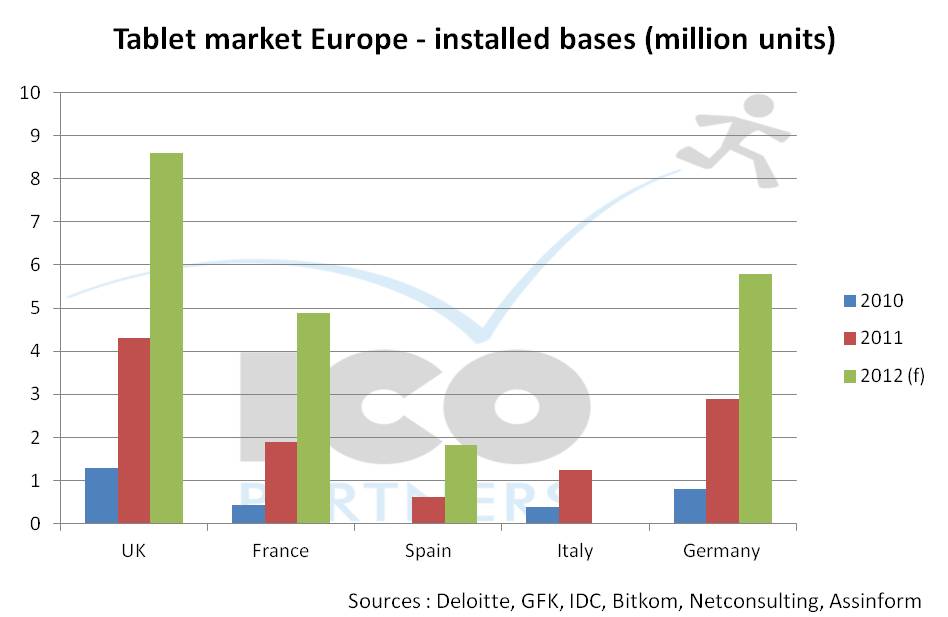

Examining public data from IDC and Gartner that I have seen so far seem to place the total EMEA tablet shipments to date at the end of Q1 2012 to about 30 million, which should amount to an installed base of around 25 million. That seems to be confirmed by this report from Futuresource Consulting, which pins the installed base for tablets to 18 million in Europe at the end of 2011 (a bit less than half the US number at 37 million.)

Regarding individual countries’ installed bases, I was able to find the following data :

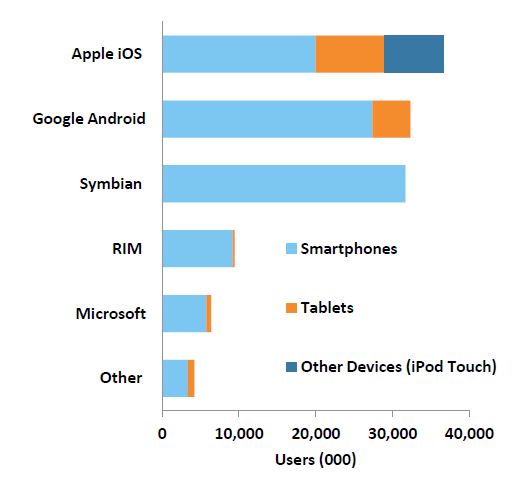

A bit more info about the tablet market in Europe, Amazon’s Kindle Fire is not available on the Old Continent yet. According to Comscore, the OS breakdown is as follows :

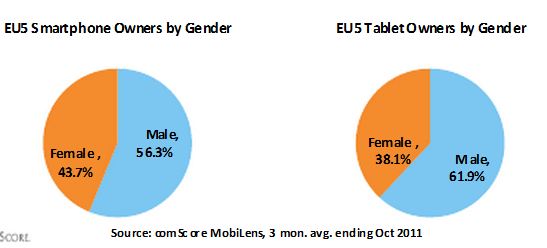

Regarding demographics, tablet owners in Europe are mostly male (62%), in greater proportion than smartphone owners. 42% are aged 25-44.

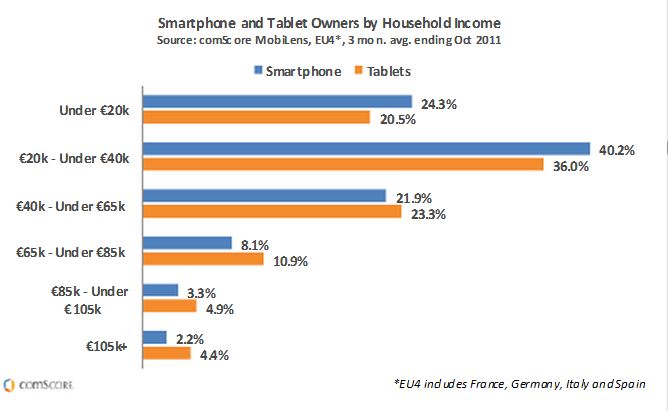

In terms of income range, most of the tablet owners have revenues comprised between 20 and 40k€ yearly, which shows that the devices are not reserved for the high incomes, although they remained a bit more skewed towards high incomes than the smartphones:

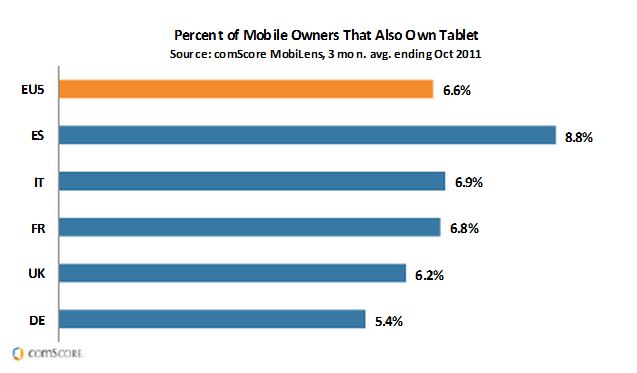

In terms of cross-platform ownership, Spain is ahead, followed by France, UK and Italy :

We all managed to avoid the GDC flu but are still pretty quiet for now, waiting for a time when the workload eases up and we can blog more frequently again. TO hold you over a bit until then, here are the presentations from the lectures Diane and I delivered during the week of the GDC.

In chronological order, here are the slides from my presentation during the Social and Online Game summit of the GDC:

View more presentations from ICO Partners

I ran out of time and couldn’t cover the case studies in the end, so even if you attended you should find a few extra details in here.

Diane lectured on Business Models: current trends and perspective for the future. She didn’t run out of time, and some of the slides don’t speak for themselves very well, but you may still find the presentation useful:

View more presentations from ICO Partners

Questions or feedback? Please let us know!

I am very late in relaying the information but, like every year, we will be in San Francisco for GDC next week. Team GDC will be comprised of Diane, Jen and myself, and if you want to meet with us we still have room to fit a few more meetings. Just contact us.

I am very late in relaying the information but, like every year, we will be in San Francisco for GDC next week. Team GDC will be comprised of Diane, Jen and myself, and if you want to meet with us we still have room to fit a few more meetings. Just contact us.

You are also very welcomed come by my lecture during the Social and Online Games Summit where I will talk about the “Keys to the European Market” – this is a 25mn lecture, I will need to go straight to the point and won’t have much time for question afterwards but you are more than welcome to grab me after the session.

Diane also has lecture at the Game Connection America held in parallel where she will discuss “Business models in games – trends and prediction“.

We are all very much looking forward to being there and inhaling a large dose of inspiration about the industry’s future.

A quick chart I built that can be a good addendum to my last post about the online gaming trends in 2012:

Also, a friend on Facebook noticed that I didn’t even talk about console games in the trends, which is true. My answer would be that it’s still very difficult from an operational and business point of view to run 100% online games on the current gen of consoles, and that the console business this year is likely to be suffering in at least some parts of Europe as the retailers struggle, so there isn’t much money and effort invested there. There’s a good article today on Gamesindustry.biz about that.

If you have been following our activities, you may be aware that we started up a media relationship management service (also called ‘public relations’/PR) called ICO Media in 2010. We recently added a new section to our website to outline our approach to media relations for online games.

If you have been following our activities, you may be aware that we started up a media relationship management service (also called ‘public relations’/PR) called ICO Media in 2010. We recently added a new section to our website to outline our approach to media relations for online games.So… ICO Media in 2011 was very interesting for us. We took on more PR clients, and the team had a greater variety of tasks to juggle than in the previous year. We experimented with tools to improve efficiency, learned a lot about what works for us, and streamlined our processes quite a bit.

We had to keep an ever-present eye on our resources in order to keep with the demand from clients, while at the same time maintaining the core elements of our service, which make us unique: we liaise with media throughout Europe; communicate on our clients’ behalf with a long term, sustainable perspective; and work with peripheral media that have a relevant focus in line with our clients’ games. Here come the numbers (a few more than in the last post):

– 8 different clients: 4 short term missions that ended during 2011, and 4 longer term contracts (of six months or more), all of which are currently ongoing. Four longer term contracts is really the limit for the size of our present team.

– 34 high level press releases sent to the media in English, plus 120-some localized versions. We also sent 75 lower level ‘news alerts’ over the course of 2011, which were timed to deliver key info and announcements promptly without becoming spammy.

– We reviewed and collected close to 10 000 articles published by European professional and enthusiast press in connection with the news we distributed.

– 29 reports were submitted to clients. This includes both end-of-mission summaries and the monthly reports we provide to our longer-term clients. Our reports include statistical results, press feedback, analysis and recommendations. A lot of work goes into our reporting, and we feel that’s a huge part of our value to clients.

– 247 press meetings were pre-booked for gamescom (B2B) on behalf of our 4 long-term clients. This is the number that intimidates me the most, because I am not sure we will ever beat it! Unless of course we include all the walk-up appointments we book during this year’s show in our 2012 retrospective. ![]()

Really we know that numbers are just numbers, but these particular ones make us happy. Considering that our PR service will be just 2 years old this spring, we’re proud of what the team achieved last year and how far we’ve come in such a short time. Now we’re immersed in this year’s work, and excitedly approaching some new frontiers.

Watch this space!

If you would like to know more about ICO Media and our approach to media relations, please get in touch.