It has already been six months since my last check on the crowdfunding trends for video games. With everyone taking it slow because the summer is coming (I am joking, everyone is rabidly preparing for gamescom), here is the latest data and what I make of it. This is part one, as I will do another blog post on Tabletop Games. Read more

Like last year, I did a mini-research on games on Kickstarter at the mid-year point. It allows me to keep an eye on any trends, and to check hard data properly a little more often. On top looking at the Games category and the video games and tabletop games sub-categories, I am also throwing in a few numbers on Kickstarter overall.

As a side note, it was interesting to see that our Campaign Review service has been very popular this year, and I updated the page about it.

A few disclaimers on this article and the data:

A significant change I have made in my methodology is to use different exchange rates. I used to have a fixed exchanged rate applied to all projects. I now use the average of a given year. It will have an impact on the numbers you saw in the past.

I use the term Semester for a half year, from the Latin semestris, “of six months”.

Data is, as usual, collected with the help of our friends at Potion-of-Wit.

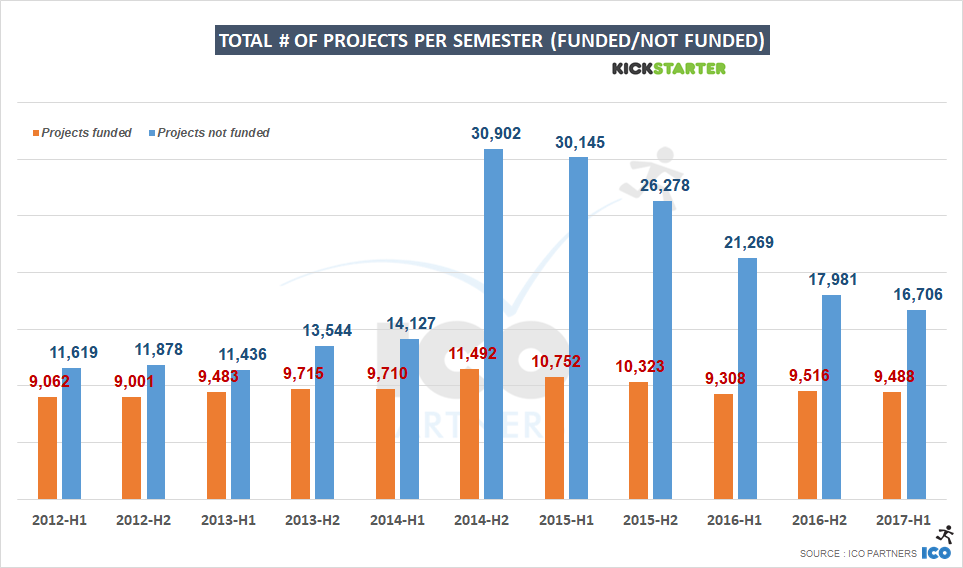

Kickstarter Overall – a steady course

Before we get into the numbers, I wanted to highlight a few things that have happened in the first half of the year:

As a Public Benefit Corporation, Kickstarter has released its first annual Benefit Statement. It is a very interesting read.

Kickstarter launched the Hardware Studio initiative. It comes on the heels of increasing reports of Kickstarter projects being copied and beaten to market.

Guest Pledging was introduced, allowing to back a project without having to create a user account.

And lastly, but more anecdotally, Yancey Strickler, the current CEO of Kickstarter, is looking for a replacement.

The last one I wanted to highlight as I sometimes find my research in media discussing Kickstarter, and they came up quite significantly in relations to that last announcement. But to the numbers, that’s what is of interest here.

As I have mentioned in the past, the Potato Salad campaign had a huge influence on the number of projects submitted on Kickstarter. If you are wondering about that sudden spike in the second half of 2014, that’s why.

Overall, we see a decline in the total number of projects launched on the platform, on quite a steep curve. However, the number of projects that get funded is seeing a very small decline in comparison. It’s also important to note that there are indications that the second half of a year usually performs better than the first half. And that’s usually true across all the categories.

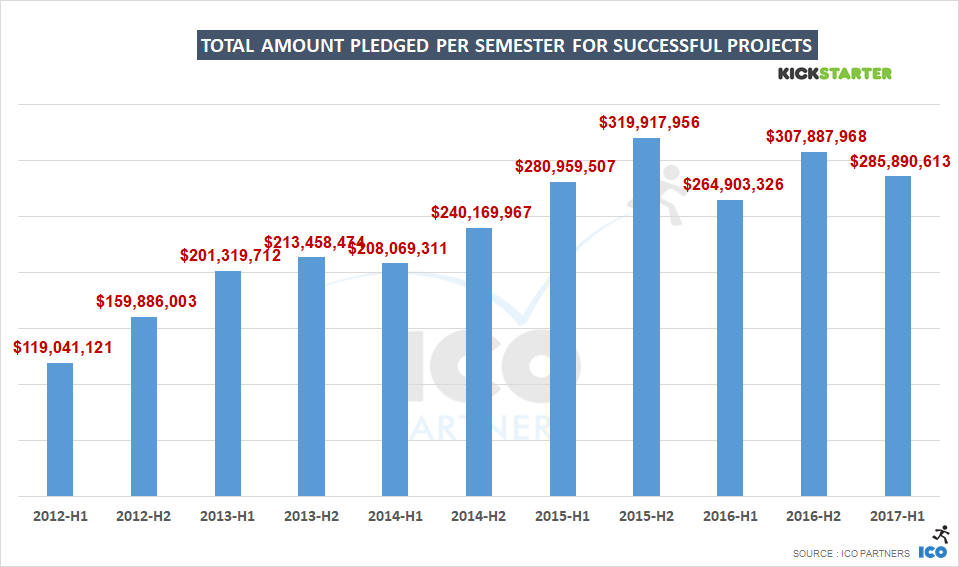

You can see this effect a bit in the total amount of money raised by successful projects:

Despite the slight decline in projects, the first half of 2017 has been the best first half for the platform historically. It is very hard to predict how the second half will go, but it is likely that it will outperform the second half of 2015, making 2017 a record breaking year, improving from 2016.

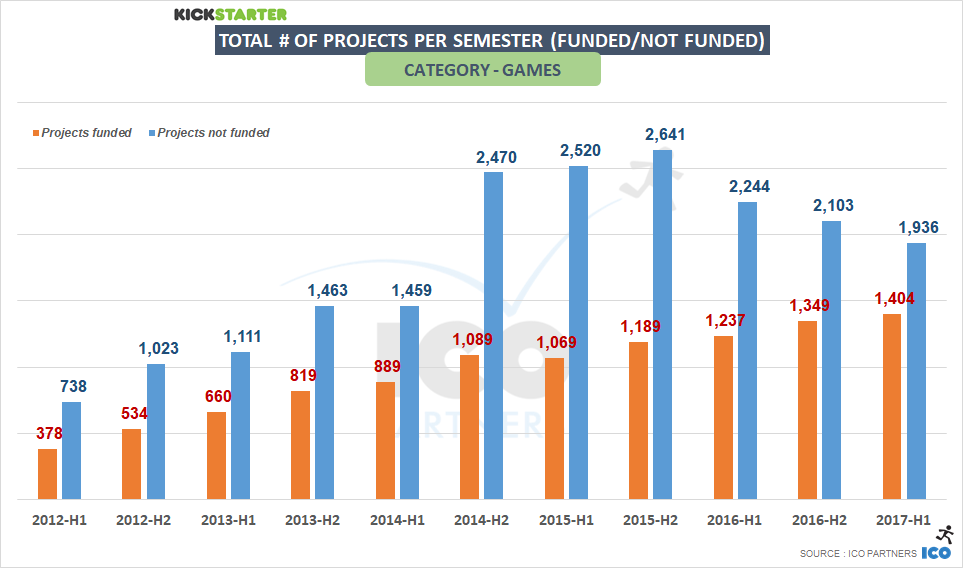

Quick look at the Games category

I will share these numbers and chart as is. The analysis of the two main subcategories are much more telling of the current trend.

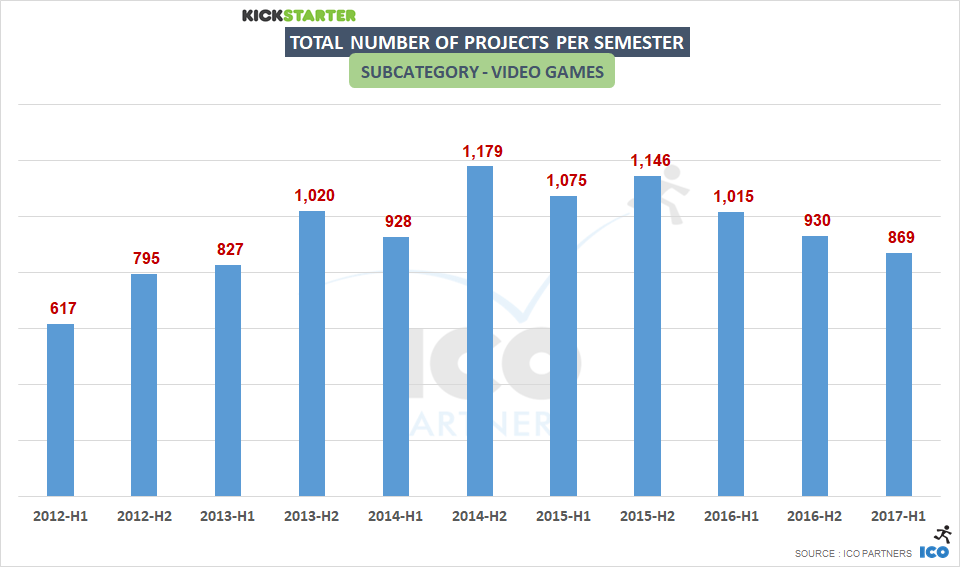

Video Games – at a stable pace

You have observed the growth of the Games category? Well, video games are actually not growing.

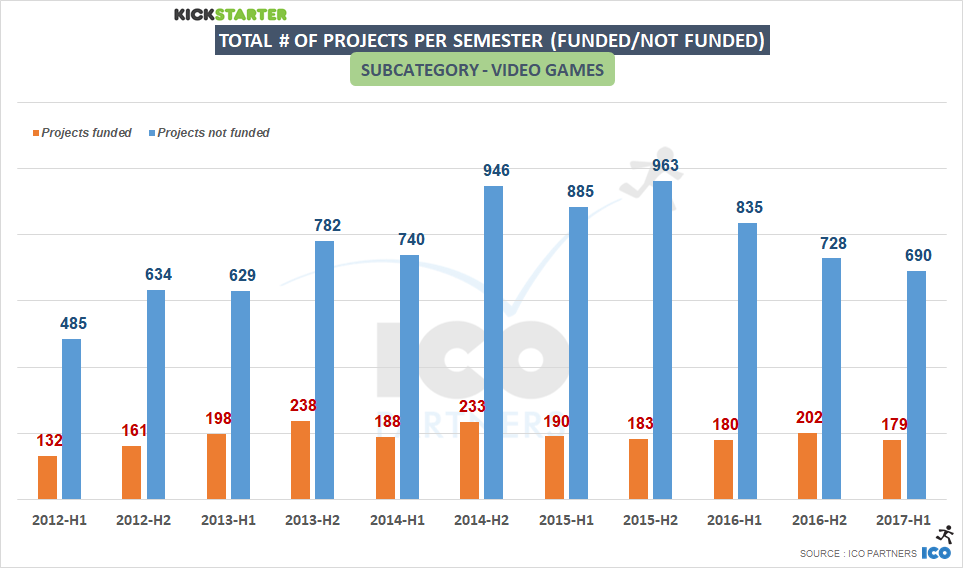

Video Games are keeping the same rhythm as the previous year, with roughly 30 projects per month getting funded. The second half of the year should probably see a few more projects funded than have been so far in 2017, if it follows the pattern of previous years.

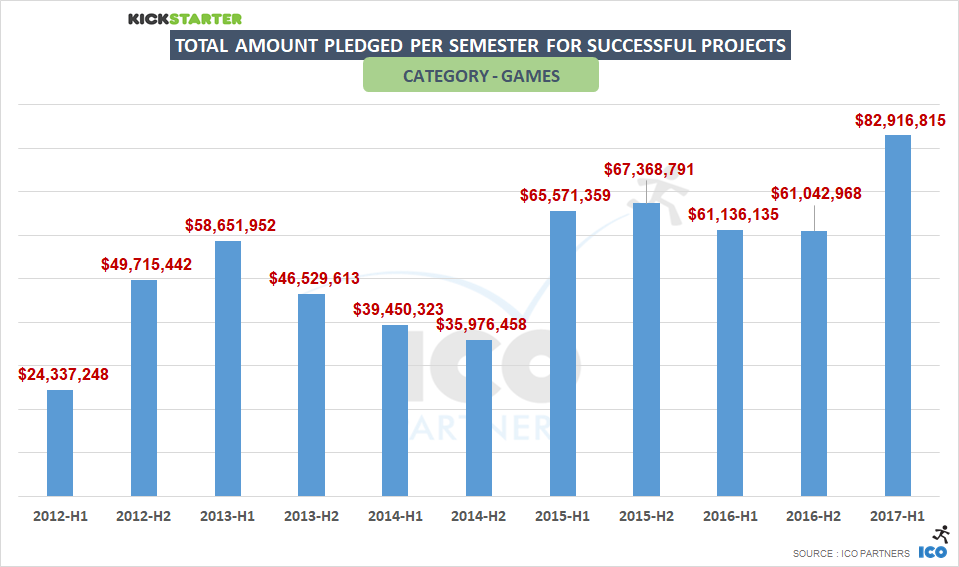

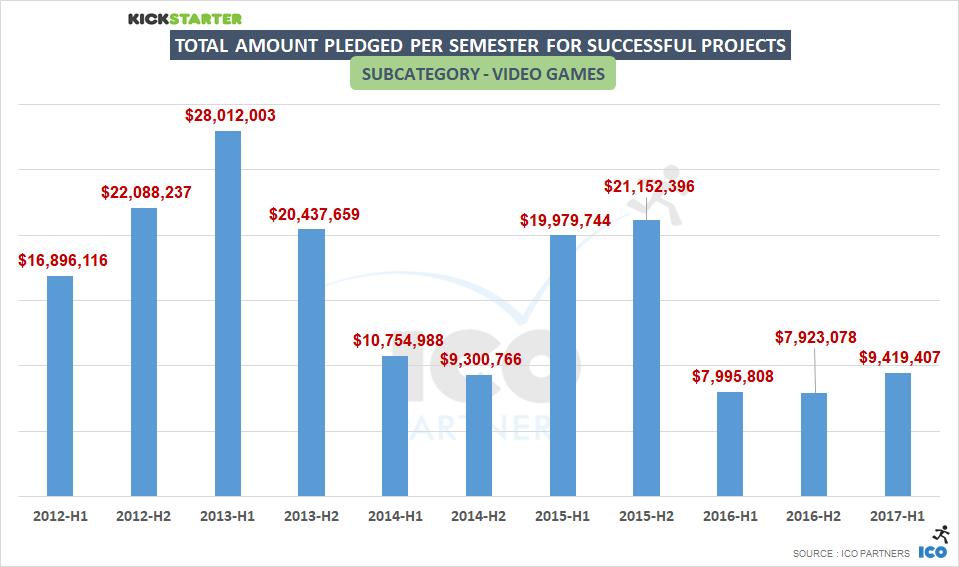

As seen in the past data analysis, the Video Games subcategory is very dependent on hits when looking at the total amount of money raised. In that sense, the first half of 2017 has been the best semester since 2015. And yet, this is a far cry from the best semesters in that subcategory.

A stable number of funded projects, a growth in the total amount raised, despite Kickstarter having lost its novelty years ago now, it is still a platform that is consistent as a source of funding for games, the same conclusion drawn on the blog post from the beginning of the year.

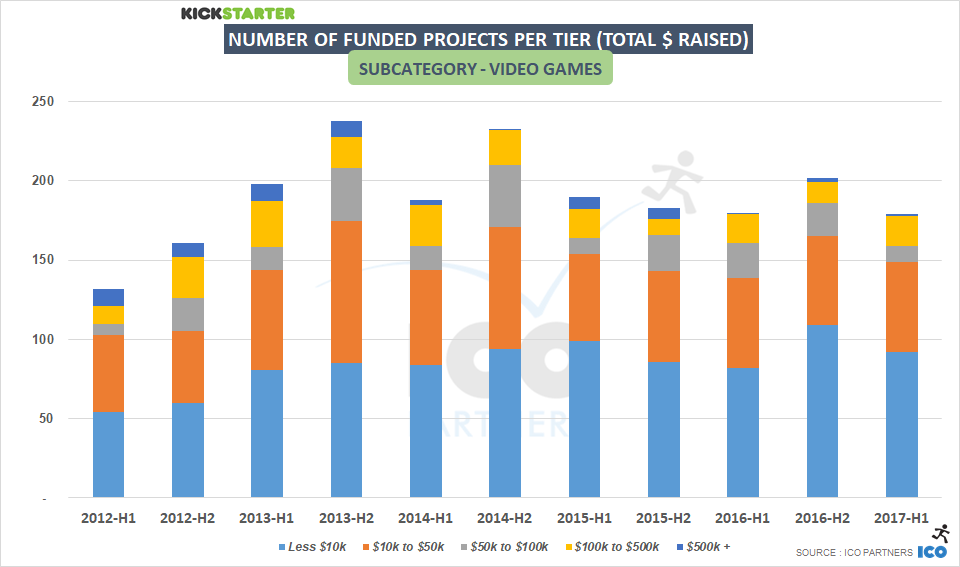

An interesting evolution of the numbers when looking at projects tiered by amount raised, there is a growth of the number of projects raising between $100k and $500k recently. It seems this is a range of funding that is more accessible than it used to be, and could be where Kickstarter could grow its Video games subcategory.

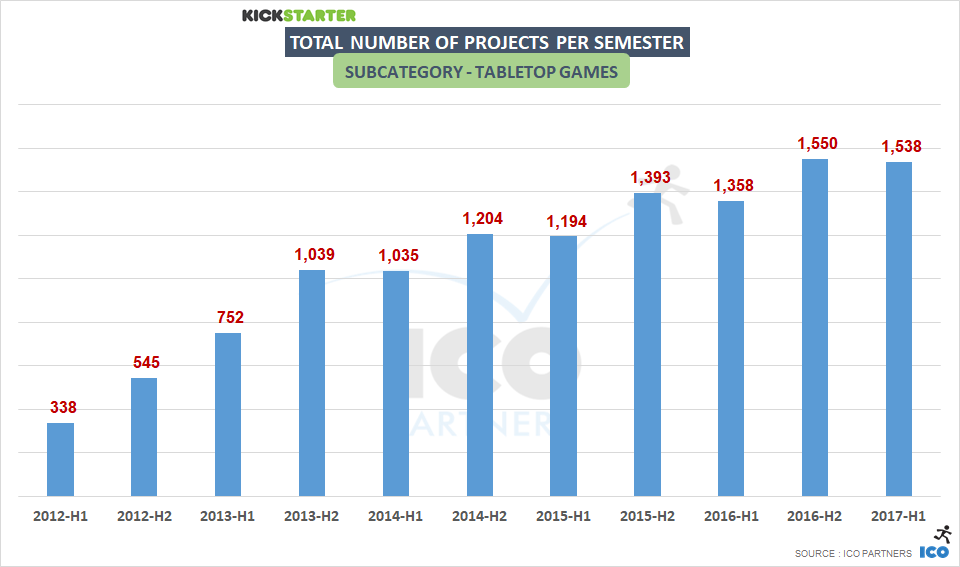

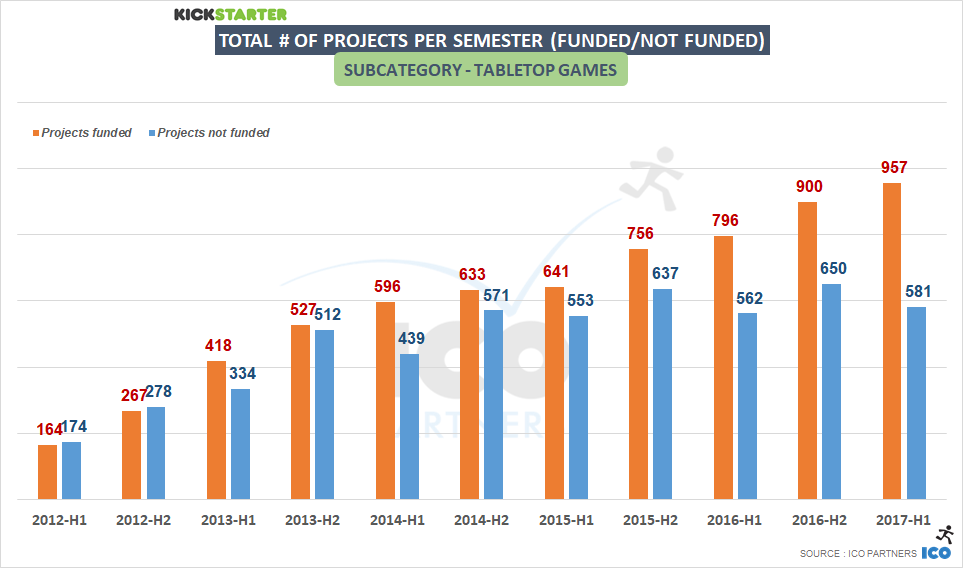

The crazy growth of Tabletop Games

If we can’t see how the Games category can be performing so well from looking at Video Games, it probably means that Tabletop Games are doing incredibly well. That is quite the understatement:

Looking first at the number of projects, it is obvious that this subcategory of projects is bonkers:

There is a strong and steady growth of the number of projects that are funded.

There was no “potato salad” speculation effect in the second half of 2014 (at least, not as visibly as in other parts of the Kickstarter platform).

The number of projects failing is stable, meaning the success ratio is steadily increasing (62% of the projects got funded in the first half of 2017)

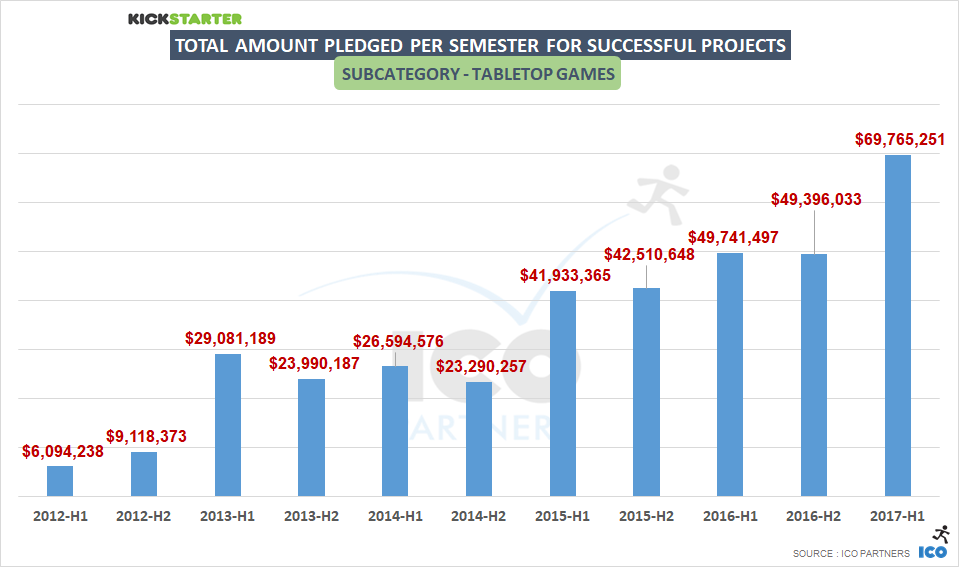

Following the steady growth of funded projects, it is not surprising to see a record breaking half-year, and if current trends continue there is no way that 2017 is not going to be the best year ever for the subcategory too.

Let me share the number that I find the most mind-boggling in the mid-year update:

24% of the money raised by successful projects on Kickstarter were Tabletop games projects

Of course, the huge success of Kingdom Death Monster 1.5, that raised $12.3m, plays a role in that impressive performance. But the growth is seen across all the strata of funding:

Across all tiers (except the lowest one) this was a record breaking semester in the total amount of money raised.

Conclusion

With board games growing so fast, and the rest of Kickstarter being still quite stable, it is clear there is a shift not visible at a first glance on the platform. There is a slight decline, or at best stability, across all categories, with the exception of one that keeps growing steadily.

By the time Kickstarter has found its new CEO, I can easily imagine games representing a third of the money raised through the platform.

And Games projects might be blurring the line between tabletop games and video games further, like the currently live campaign of Beasts of Balance:

https://icopartners.com/newblog/wp-content/uploads/2014/03/kickstarter_header.png256710Thomas BIDAUXhttps://icopartners.com/newblog/wp-content/uploads/2020/04/CRUSHCREATIVE_ICO_BRANDING_LOGO_NavyWhite-01-e1586189748878.pngThomas BIDAUX2017-07-31 23:39:162017-08-01 12:55:36Kickstarter and Games - 2017 mid-year status update

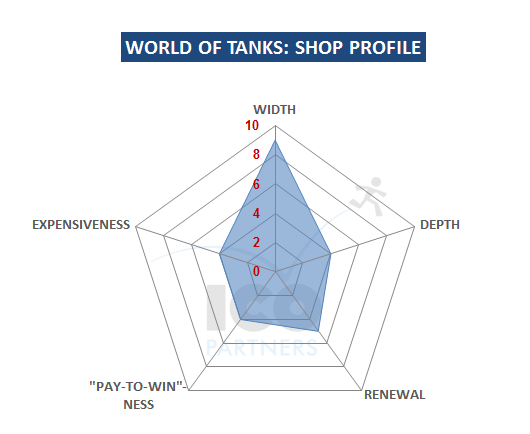

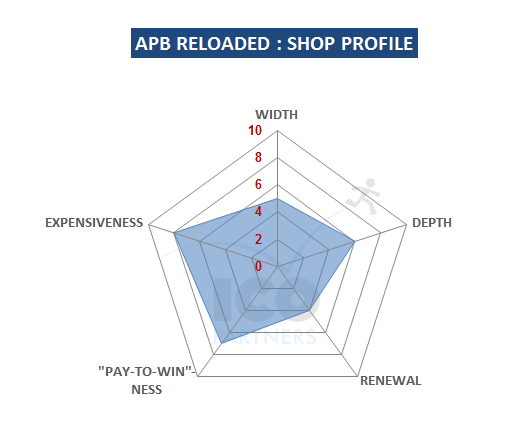

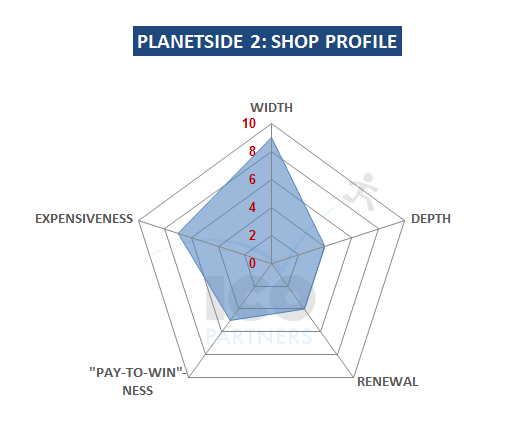

Available now is our latest report. This time around we are analysing PC Free-to-Play shooter games. I am always tempted to say it is about FPS games, but there are a number of games in that list that are not in the first person.

The report provides an overview the market as a whole before going into specific, country-to-country market data and then even further into a game-per-game analysis. We took the individual game analysis a level further, and specifically analysed each game’s F2P mechanisms and the way their stores function – including the ways in which games are managing soft currency and the hard currency.

Below are a few samples of the additional graphs we generated, using the additional information on the way the games’ stores function.

Have a look at the table of content for more details on the report. It covers 15 titles across 178 pages and costs £4,000 (incl. tax):

https://icopartners.com/newblog/wp-content/uploads/2015/04/ICO_FPS.jpg256710Thomas BIDAUXhttps://icopartners.com/newblog/wp-content/uploads/2020/04/CRUSHCREATIVE_ICO_BRANDING_LOGO_NavyWhite-01-e1586189748878.pngThomas BIDAUX2015-04-20 11:00:022016-12-23 19:47:44New report out: F2P PC Shooters in Europe

About a year ago we released our in-depth market report on MOBA games in Europe. As we are working on new projects at the moment (if you are really curious, feel free to catch us during GDC and ask in person), we want to give the opportunity for a larger audience to access some of our previous work, so we are experimenting on this front through a time-limited sale on that report.

Until the 6th of March, the MOBA games in Europe report is available at an 85% discount, from £2,200 to £300. Just go to our Gumroad page and enter the discount code wintersale2015. Read more

Available now is our latest market report. We have taken an in-depth look at the MOBA sub-genre, specifically its presence on the European markets. This is an extensive report, looking at each game as well as every single market, and drawing an interesting picture of the current trends in the genre.

With an estimated revenue for all the games in Europe of €173m ($237m) for 2013, MOBA games have been growing very rapidly in the past few years and should continue to develop for the foreseeable future. Below, you can find the foreword to the report as well as the table of contents. As usual, don’t hesitate to contact us if you have any questions.

The MOBA genre is still in its infancy. Born out of the Warcraft 3 mod community with the Defense of the Ancients map, it was a genre limited to that space for many years. As this community grew it reached a critical point that either prompted game studios to consider the genre as viable for a stand-alone game, or the community matured enough to take their expertise from modding into full game development.

The definition of the MOBA is still evolving. Like any newly created popular terminology, its usage will vary from person to person until it reaches a point of compromise (or academics dissecting the game landscape narrow down a very specific definition). We have decided to stick to a rather strict definition for this report and only integrate the games that have directly inherited from the Defense of the Ancients core mechanics: players in teams each control a powerful unit and try to outplay the opposing team by controlling the flow of a battle, destroying objectives or simply killing the enemy players’ units. For players, the main appeal of a MOBA lies in the depth of gameplay: the numerous units available, the number of development options for those units and the understanding of the different match-ups to react to the opponents’ decisions. It also means these games are very competitive, require a great deal of time to be properly mastered and have created communities that are highly engaged, yet passionately demanding and not always tolerant (one could say toxic).

However it is that passion from the players that it is a contributing factor in MOBAs emerging as a major genre at the moment – and the audience of those games is equally demanding when it comes to the quality of the games, making it a difficult genre to enter. It doesn’t appear to scare new entrants though. As we finalised this report earlier this year there, came a point where we had to stop adding titles to the list of announced MOBAs as these new game announcements were being made on a weekly basis. We feel this report is being released at a very interesting time for the genre. It will allow a line to be drawn in the sand, and a snapshot to be created for the state of the European MOBA market. And it should help us (and you) see where the market will go from here and how this new genre will develop and grow.

https://icopartners.com/newblog/wp-content/uploads/2014/02/moba-report_blog.png256710Thomas BIDAUXhttps://icopartners.com/newblog/wp-content/uploads/2020/04/CRUSHCREATIVE_ICO_BRANDING_LOGO_NavyWhite-01-e1586189748878.pngThomas BIDAUX2014-02-18 10:44:442014-09-23 16:26:56New report out: MOBA games in Europe

We are very happy to announce that we have released our first market report directly available on the website. This is a very specialised report as we looked into client-based MMORPGs specifically, with a deeper look on how they perform in the largest countries of the region (UK, France, Germany, Spain, Italy and Poland).

Here is the top-level bullet points on what you can find in it:

● General overview of the market: global size of the market, respective size of the key countries, business models popularity.

● Key data for the main countries: market size, preferred payment types, most popular games per language.

● List of the client-based MMORPGs in service Europe.

● Profile for each publisher with estimated revenues.

If you are curious about it, I strongly recommend to have a look at the table of contents of the report, and Joost from SuperData Research (we partnered with them on that report to make the research as complete as possible) has an article with a few key insightsfrom the report:

● The client-based MMO market totalled $1.3 billion across its major markets in 2012.

● Three publishers dominate the space, generating 70% of all revenues.

● Germany is the largest European client-based MMO market with €474MM in 2012 sales, more than double the size of the UK market (€281MM) and France (€222MM).

Since the inception of ICO Partners, it has always been our objective to provide more than our usual bespoke reports that we build for our clients. It took us some time to get to the point where we were able to build that first market report, and Diane has spent all her time for the past few months on it. Now that it has arrived, we have other segments of that market that we really want to dig into. You can expect more content on the Publications section of the website this year.

https://icopartners.com/newblog/wp-content/uploads/2013/02/report_MMORPG.png256710Thomas BIDAUXhttps://icopartners.com/newblog/wp-content/uploads/2020/04/CRUSHCREATIVE_ICO_BRANDING_LOGO_NavyWhite-01-e1586189748878.pngThomas BIDAUX2013-02-04 11:09:422014-09-29 09:53:47New report out – Client-based MMORPGs in Europe