Virtual Worlds Management has posted its update on Youth Virtual World sector. If it seems to you that the sector is crowded, it’s probably because it is : they numbered 200+ of them. Read more

Virtual Worlds Management has posted its update on Youth Virtual World sector. If it seems to you that the sector is crowded, it’s probably because it is : they numbered 200+ of them. Read more

With a new year starting, it is time for two customary types of blog posts: retrospectives and new year wishes. Here, I have decided to combine them both for you.

Considering how much time I have spent looking at and talking about Kickstarter data, it would be a shame to miss the opportunity to join the crowd of analysts of the platform in giving my own take of the past year – with my usual focus on games in general, video games specifically.

[reminder – for the purpose of our data analysis, we re-qualified the Ouya as a Technology project]

2013 and Kickstarter

In 2013, there has been $477m pledged on Kickstarter, across close to 45,000 projects. About 20,000 projects got funded this way.

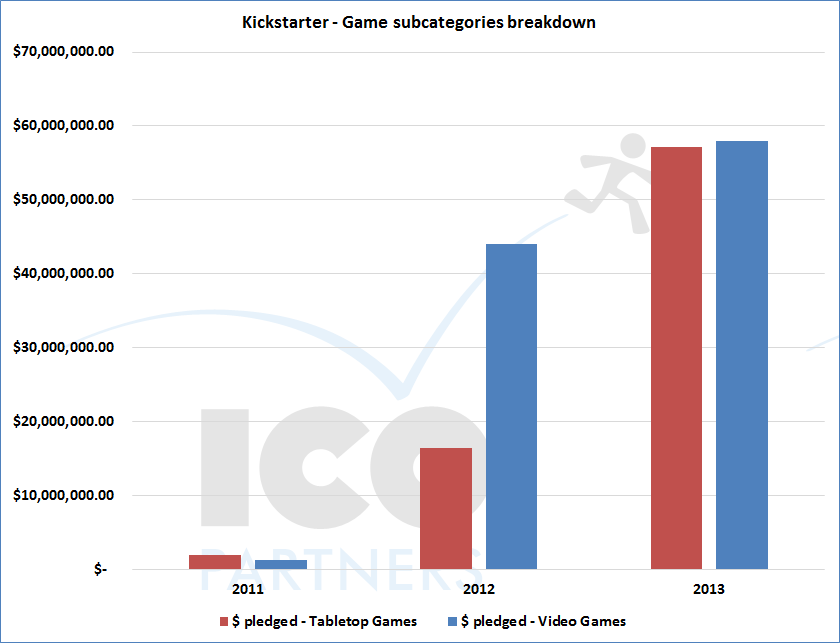

Games represent the largest category on the platform, in front of Films, and by a large margin.

Video games in 2012 and 2013

2012 was a remarkable year – it saw the Double Fine Adventure project put Kickstarter on the map for independent video game developers all over the world and the number of video game projects explode on the platform. From $1.2m pledged in 2011, Kickstarter went to close to $44m in 2012.

Throughout that year, a number of projects reached very impressive numbers for their funding and 2012 can be seen as Kickstarter Year One for video games for sure.

So what about 2013? We saw that games as a category did very well, but you have to account for the fact that the category itself accounts for both video games and tabletop games projects.

Yep, that’s right. Tabletop games represent almost half of the money that was pledged for games on Kickstarter in 2013. Being a board gamer, it makes me incredibly happy. But more on this later, I will keep looking at video games for now.

2013 was to be a key moment – would the trend of growth continue and was it going to be steady? Or was there to be a collapse as the first large projects got delivered and a certain fatigue for crowd funding crept in?

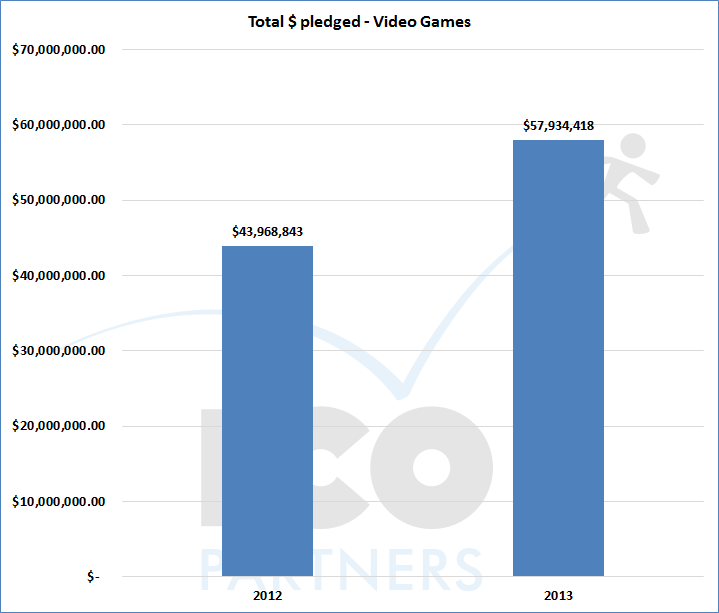

Purely looking at the total of money pledged for video games projects, it is obvious that 2013 was a better year than 2012. About 30% better. But such a snapshot can be a bit misleading – 2012 had a slow start with the Double Fine Adventure explosion happening after February.

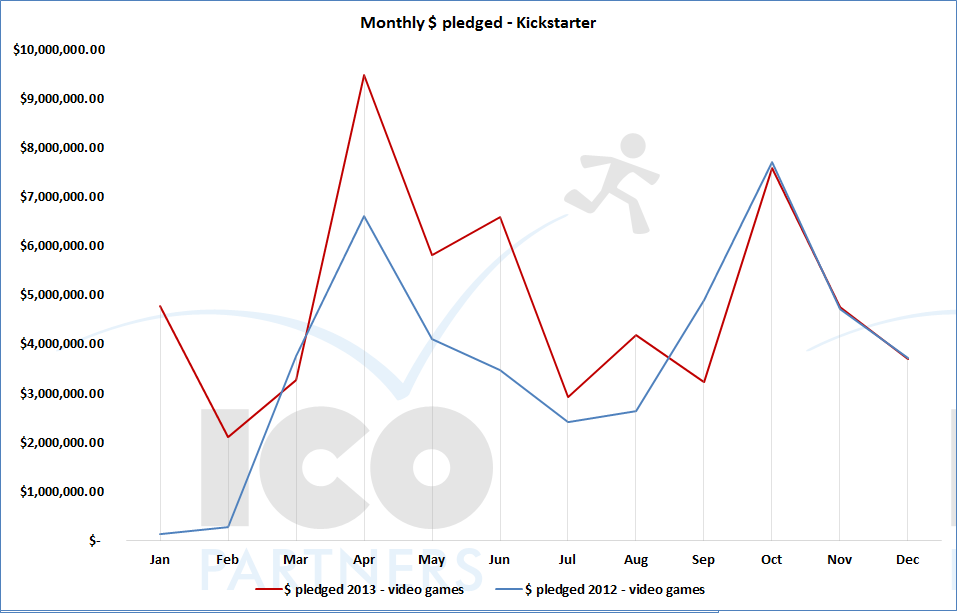

Looking at 2012 and 2013 month-by-month is interesting: you see that the end of 2012 and the end 2013 had almost the exact same volume of money being pledged. The difference between the two years mostly happens in the first half. It is not a big stretch to imagine that a plateau has been reached and that variances are created by the “hits” (post $500k projects). And, to be honest, I am less interested in those large project performance than I am by the potential of the platform for small projects.

For Kickstarter to get a foothold in the game industry as a source of funding of interesting projects, we need to see projects of all kinds being successful on the platform.

{kind=link}

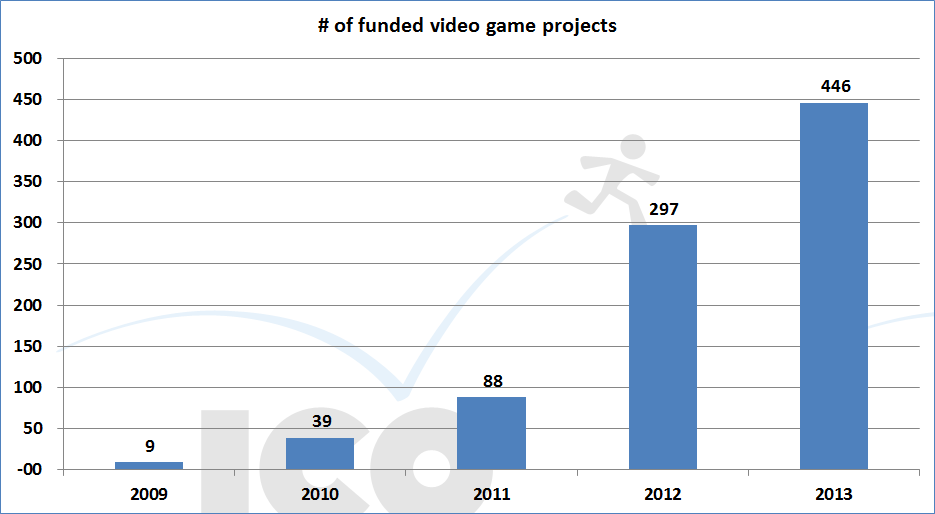

It is reassuring to see that a similar number of projects funded in 2013 compared to 2012, and a much better indicator to see if the model is sustainable.

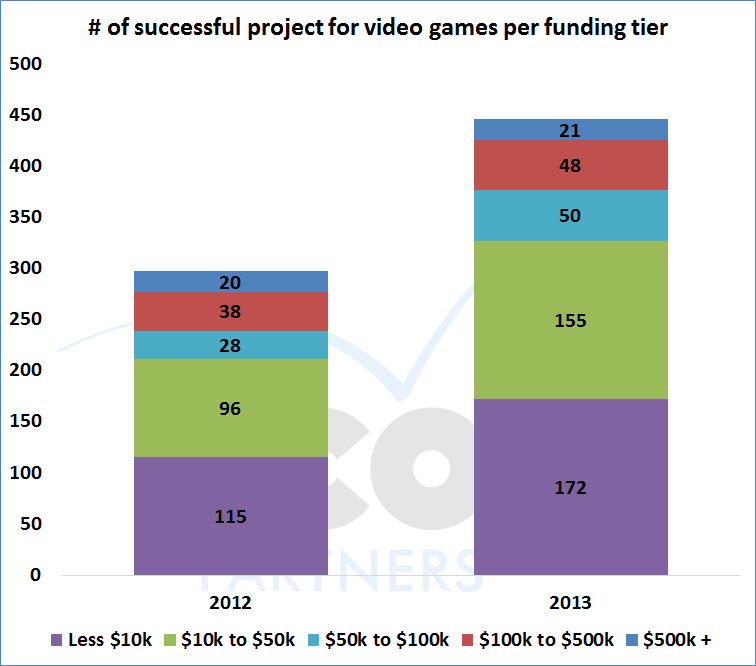

The following graph shows the number of successful projects per “funding tier”. The funding tiers are based on the amount of money the project raised and were empirically set by me. I think they represent meaningful tiers for independent games budgets.

So basically, between 2012 and 2013, the number of $500k projects is essentially the same (around 20), but there has been 25% more projects raising between $100k and $500k. 80% more projects raising between $50k and $100k, 60% more projects raising between $10k and $50k and 50% more projects raising less than $10k.

And to me, this looks like good news overall. It shows a wider selection of projects can get funded via Kickstarter, and not just the very cheap or the very famous. I would be ok for 2014 to see fewer shiny, large projects if that would mean a larger number of projects found a way to get funded. I think this evolution stems from the development of a community of video game enthusiasts embracing the crowd funding principles. A growth from the bottom up sounds a lot healthier overall.

Some numbers

Graphs are nice, but you probably want to have some direct numbers from all this. Worry not, I am very happy to provide the ones we have (all for video games projects):

|

2013 |

|

| Number of pledges made |

1,129,522 |

| Number of projects submitted |

1,851 |

| Number of projects funded |

446 |

| Number of projects that failed getting funded |

1,405 |

| $ pledged to video game projects |

$ 57,934,417.74 |

| Success ratio |

24.1% |

In 2013, Kickstarter expanded its platform to new countries: Canada, Australia and New Zealand. And we also now have a full year with the British platform. I explained my thoughts on some reasons why this dones’t necessarily mean much, but if you want to know the repartition between the currencies, here it is:

| Kickstarter platform |

$ pledged – Video Games |

| USD |

$ 50,370,976.75 |

| GBP |

$ 5,910,926.00 |

| CAD |

$ 1,336,856.70 |

| AUD |

$ 287,084.96 |

| NZD |

$ 28,573.33 |

(Currencies converted into USD equivalent)

Tabletop games and video games

So, tabletop games got huge this year on Kickstarter:

It personally makes me very happy (and I did contribute actively to that category myself) as I love board games, but it also makes me wonder what video game projects creators could learn from tabletop game projects.

The main problems their funding is to solve are fundamentally different. Video games have a high, fixed cost (the game development) and board games have a high, flexible cost (production and shipping of those games). That’s why the crowd funding works so well for board game as they can scale their main cost based on their popularity, a luxury video games don’t have. On the other side, video games have a lot of flexibility in the way they can deliver their projects and the way they can spread their development process over time – Double Fine and Revolution both deciding to deliver their games in two parts is clearly playing to that advantage.

But I digress as I think there is a lesson to learn from the success of board games (just FYI, the success ratio of tabletop game projects in 2013 was 53% compared to the 24% of video games):

Aim for the smallest amount that guarantees you can deliver your project.

Kickstarter is a platform that is perfect for projects that don’t aim for the moon, but promise a quality experience for the amount they ask for. I get to review a lot of projects on a regular basis from video games studios since I have started blogging about the crowdfunding of games – the vast majority of them are simply too ambitious and too expensive when considering the studio’s track record and its reputation. This is not the only point of failure there is, but this does seems to be the most common.

So, if I have a wish for games on Kickstarter for 2014, it might be “be more humble, be more successful”.

Special thanks to Potion of Wit for their help in the data-mining process.

Oh, and I didn’t forget that I promised this blog to cover two purposes: have a wonderful new year, we wish you and your families all the best for 2014!

It is that time again where we wish you all the best for the coming year. 2013 is holding a lot of promise for ICO Partners, some of which we should be able to discuss soon, others that are still in early stages, and all of them quite exciting. Anyone whom I ran into last month probably knows from my raving rants at the time it was taking, but we have finally moved into our new offices. We have roughly doubled the size of the space we were in, as well as improved our autonomy. The offices are still in Brighton and very close to the train station for that matter. The details have been updated on the Contact Us page, but here they are again, for good measure: ICO Partners Office 6, 10 Fleet Street Brighton BN1 4ZE United Kingdom More news from us very soon, but meanwhile…

OUR BEST WISHES FOR 2013!!!

- ICO Partners is expanding – we are looking for a Senior European PR Executive. The description is the following :

Skills and requirements:

Graduate in public relations, journalism, marketing or related programme

-

Fluent in English and another European language

-

Minimum 3 year’s experience in a position involving contact with the media

-

Experience of people management preferred

-

Strong communication skills, both spoken and written

-

Ability to work with and analyse data

-

Self-motivation and sense of initiative

-

Interest and knowledge of online games is a plus

-

Skills and experience in online video marketing and communication (Youtube, Twitch…) is a plus

Responsibilities:

- Managing relationships with journalists in one or several European territories

- Managing relationships with clients

- Team management responsibilities based on applicant’s profile

- Writing of Press Releases and Media Alerts

- Developing and updating media lists and contact databases

- Participating in daily media relations tasks, including collection and analysis of press coverage, reporting, organization of events, working with related service providers to support projects, etc.

The job is full-time and based in Brighton, UK. Salary to be negotiated depending on experience.

If you feel you would fit the bill, please send us your CV and cover letter to jobs@icopartners.com. We look forward to hearing about you soon!

Anyone who met us at gamescom this year know that we have been working on two new reports on the game industry and we are very pleased to announce that our market research on the Turkish video game market is now available to everyone on our website.

It was a very productive collaboration with Smart N Digital Marketing whose insight in the market was essential as we prepared the report. We also received a lot of support from local actors who answered a lot of questions and shared their insight with us.

You can find details on the report content over here.

We made an infographic to illustrate some key data on the market:

It has been some time since I last checked on the progress of Kickstarter in the UK for the blog. With Kickstarterlaunching in Canada next week, it seems like an excellent time to look at the performance of the GBP projects again. I have pulled some data (from early July) and tried to get a feel for the current trend.

I like to look at things and keep them at a comparable level – all the numbers you will see here are only for the first half of 2013. As I explained in the very first blog poston this topic, the early months were not very representative of the success of the platform in the UK, so being able to look at the 2013 data should be much more telling.

The fact we now have much more complete data, I can also look at things such as success ratio and other categories of projects. It also means it is a bit of a bigger picture. To make the whole thing easier to read, I have put the larger part of the findings in a Slideshare presentation. I recommend viewing it full screen:

My concluding thoughts from looking at the current state of the two ecosystems:

– The two ecosystems are not on equal footing. The UK Kickstarter seems to suffer from being in a currency not as widely understood as USD (as this is the biggest difference from the US ecosystem) as well as from the difference of payment systems (Amazon payment in the US, Kickstarter’s own system in the UK).

– Kickstarter has grown from adding the UK ecosystem. It is quite clear as most of the successful UK projects are rather small (compared to their US counterpart), they would not have been able to go through the US ecosystem in the first place (it requires too much energy/investment for a small company), and they add up to the growth of Kickstarter overall. That growth is just significantly smaller than the one observed in the US, but it is commendable.

– It also seems that the US creators are better at understanding their capacity to raise money from the crowd and at managing their campaigns. The quite low success ratio of GBP projects compared to USD projects cannot be solely blamed on the difference between the two ecosystems. I think that, in general, GBP are overshooting for their goal – it could be that they are more honest about the amount that they need to build their project, the cost of development is more important in the UK, the Brits are not as good at getting attention to their projects, or a combination of these. I have seen many UK projects that had a fairly high goal and very few channels where to recruit backers. Now, me being based in the UK, I tend to talk to more UK creators and this could be anecdotal.

– The UK ecosystem won’t grow significantly until the option to show the pledge rewards in another currency is added or a few large projects make the leap of faith (and there is proof that both ecosystems can efficiently support large projects). Anyone looking a bit closer to the behavior of the ecosystems could conclude that any large project would be better off going on US Kickstarter. The difficulty to get into the ecosystem (set-up as US entity, set-up an Amazon account) can be overcome for the right project, with the right size, and it then become a self fulfilling prophecy: all the big projects are on the USD ecosystem, ergo, if you have a large project you should put it there. You have a few exceptions (successful Australian projects on the GBP ecosystem), but you would need more of those to counteract the current trend. Ideally, you want the project creators to go to the ecosystem that is the easiest for them and there is a noticeable gap at the moment between the two ecosystems.

The addition of Canadian projects will make the platform grow further, it will be interesting to see how projects perform there compared to the UK projects.

In the meantime, I will hopefully be able to dedicate more time to build more comprehensive graph representation of those trends.