A year has passed and it is time again to look at how the Kickstarter landscape for games has evolved over the past 12 months. Read more

A year has passed and it is time again to look at how the Kickstarter landscape for games has evolved over the past 12 months. Read more

As is now the ritual, I have done a deep dive into the Kickstarter data we gather and put together some notes for you to look at how well video games are doing for the first half of 2019. Read more

Welcome to my yearly blog post on crowdfunding and games, looking at how well games have performed on Kickstarter (and Fig) for the past year. Read more

As is the tradition, this is the follow-up from the overall Kickstarter annual review from last week, with a focus on the Games category. Again, I will talk about Kickstarter, but I shared some insight on crowdfunding across different platforms for video games in a piece on PC Games Insider.

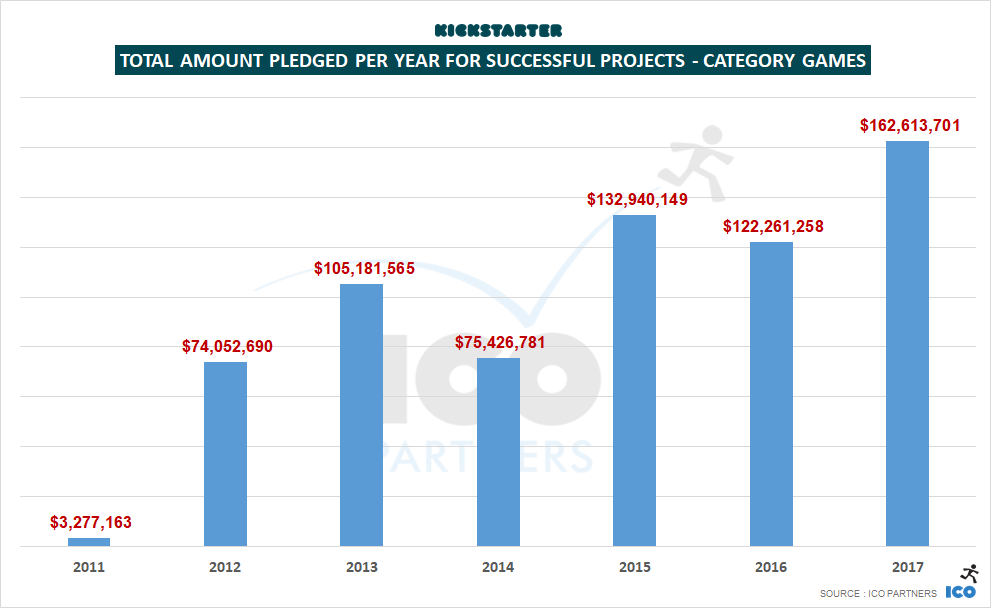

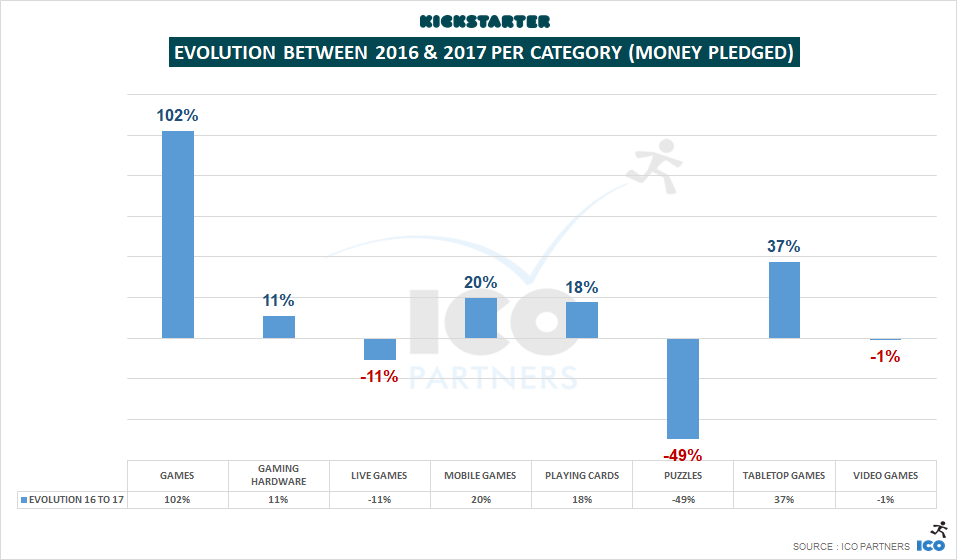

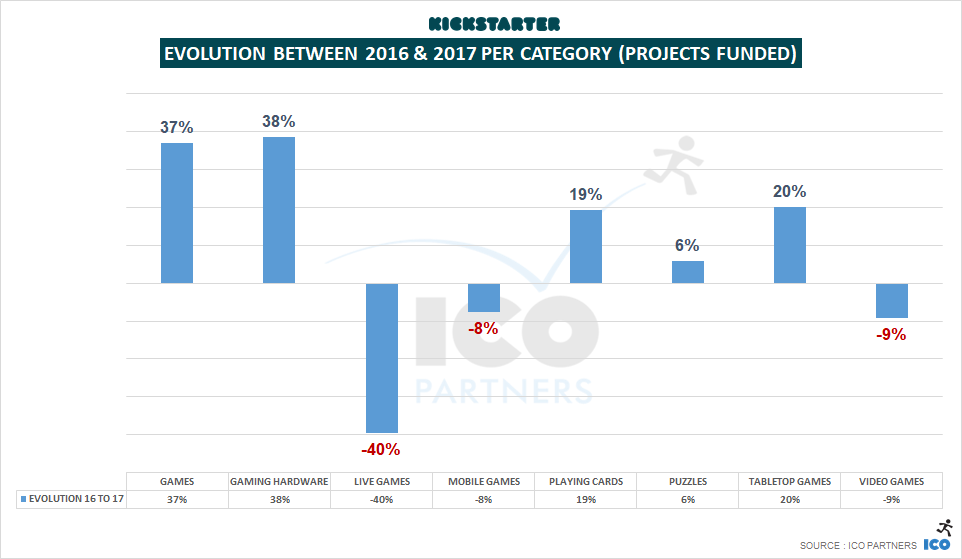

We talked about it last week, but that’s a notable change from 2016. Games represented 26% of all the money pledged in 2017, and 15% of all the funded projects.

There are two very important things to notice here.

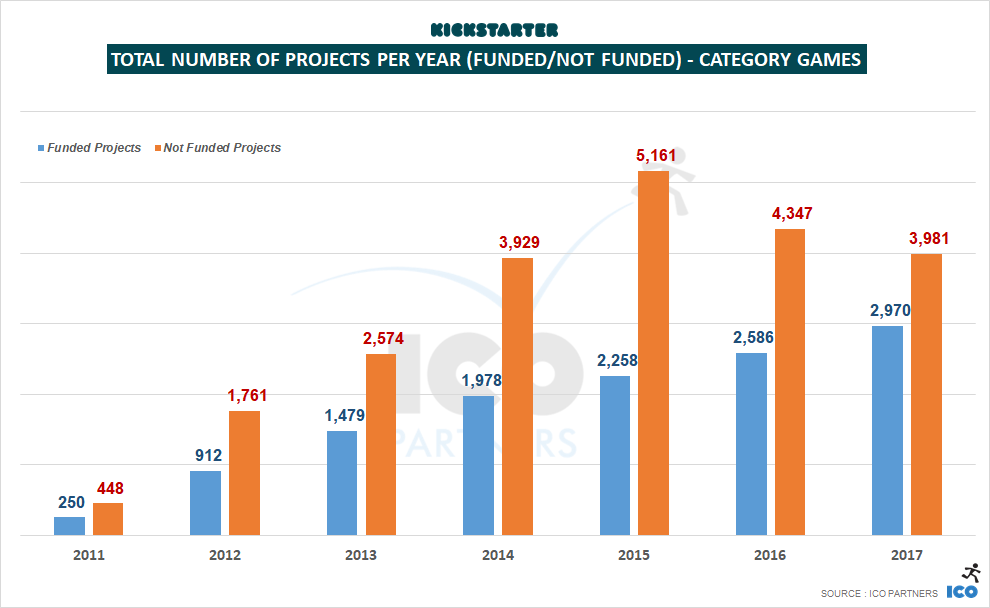

First, the overall money raised by Games projects saw a significant bump in 2017. Secondly, the total number of Games projects that tried their luck on the platform has stayed roughly the same, at just under 7,000 campaigns total, but more of them achieved their funding targets in 2017, compared to the previous year.

We can consider that the platform has reached a better maturity point, where the projects trying to get funded having a better sense of what is required to meet their funding goal. There were 15% more Games projects funded in 2017, compared to 2016.

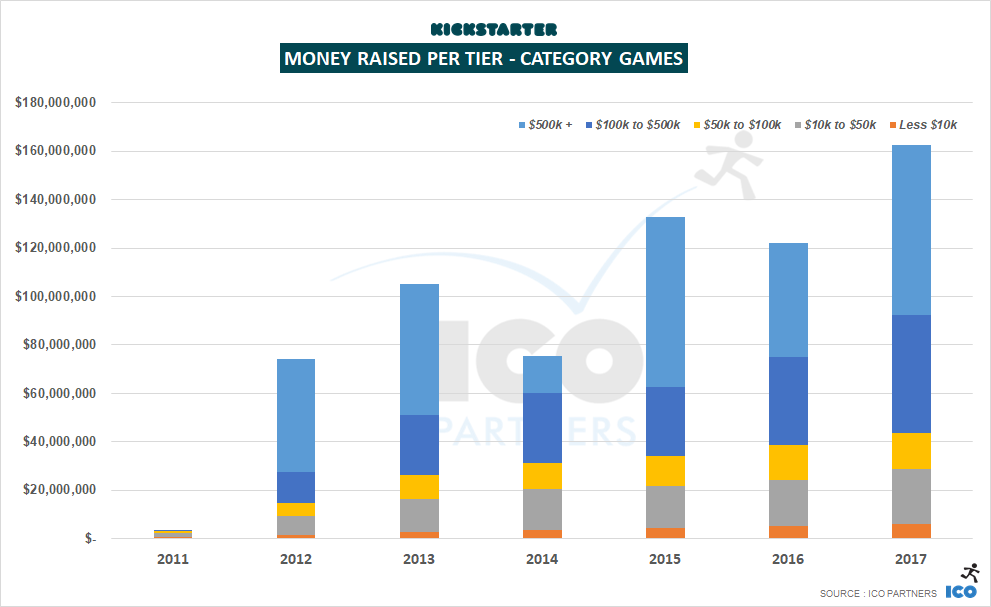

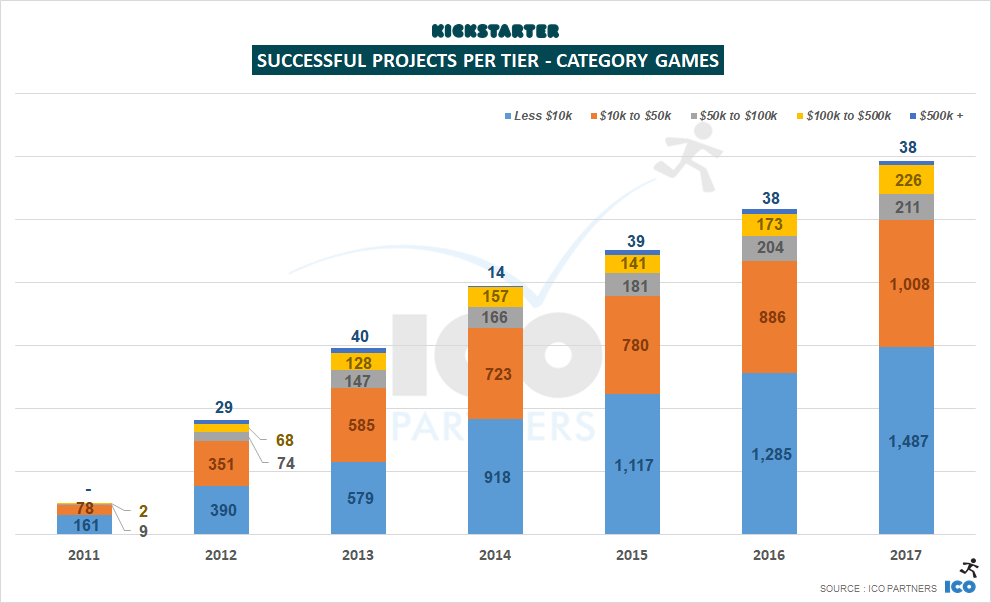

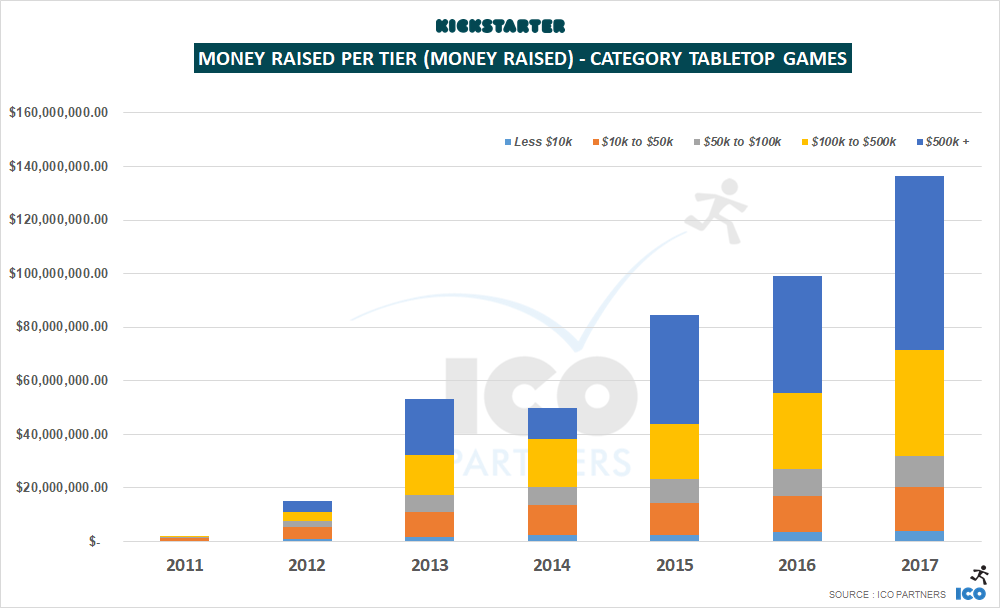

More money was raised all projects tiers. The top-tier, $500k+ projects represent a lot of the total money raised, of course – there was $70m raised by these projects alone. But the number of projects successfully raising between $100k and $500K is also up on previous years, representing about a third of all the money raised in 2017.

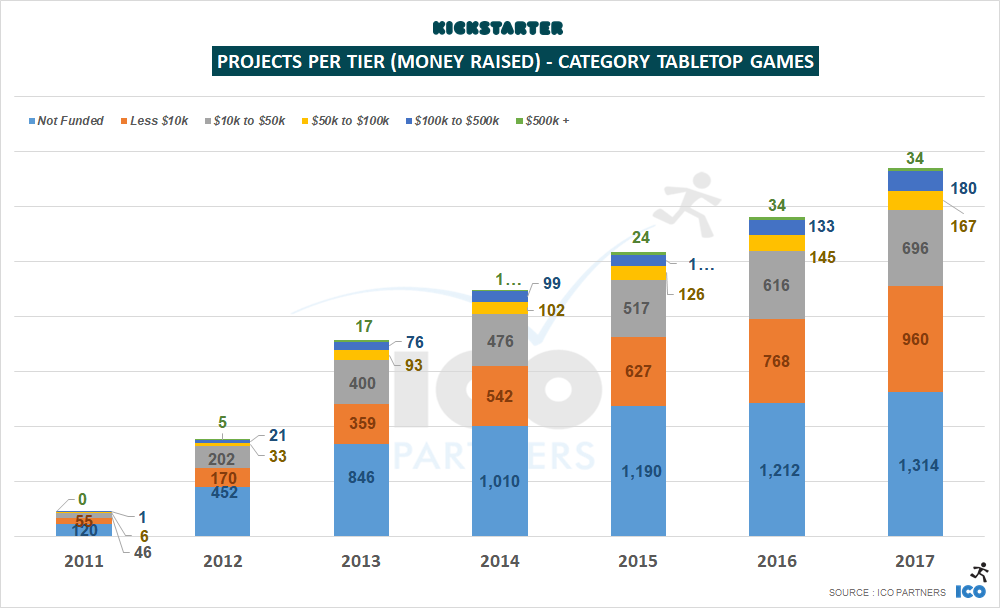

The number of projects in the top tier didn’t move from its 2016 figure – 38 Games projects raised more than $500k in 2017, the same number as the year before. A few very large projects represented a lot of the money raised. Notably, the record breaking Kingdom Death Monster 1.5, that became the #1 project in the Games category, raising $12.4m, and The 7th Continent, that raised $7m on its own. Together, these two campaigns represent more than 12% of all the money raised in the Games category, in 2017. And it is no surprise that they are both tabletop games project, and both of them are sequels/reprints of already successful Kickstarter projects.

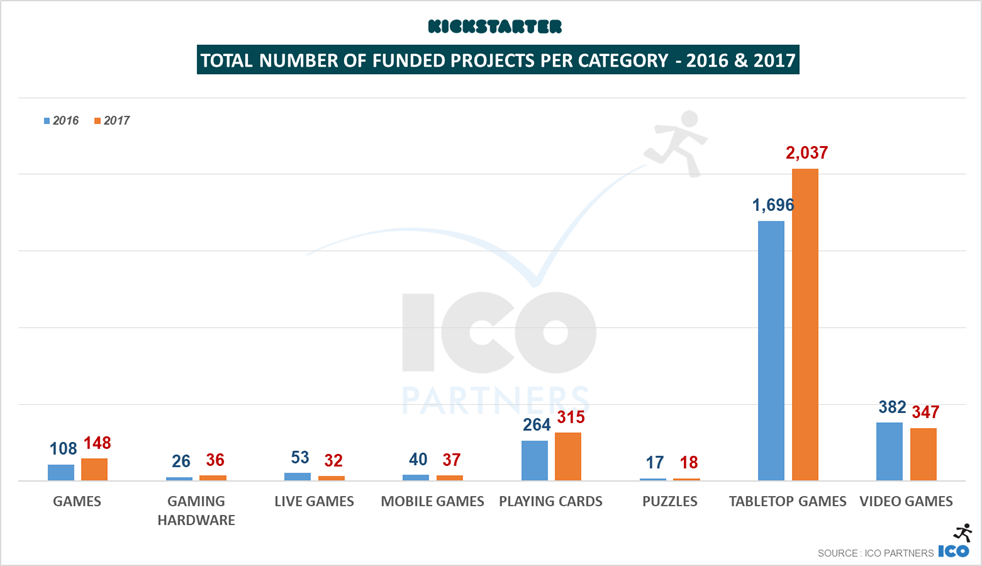

Looking at the subcategories, the number of funded projects for video games has dropped a bit from 2016. There are a few more Playing Cards projects and generic Games projects funded. But more significantly, the number of Tabletop Games projects has grown significantly, up 18% from 2016.

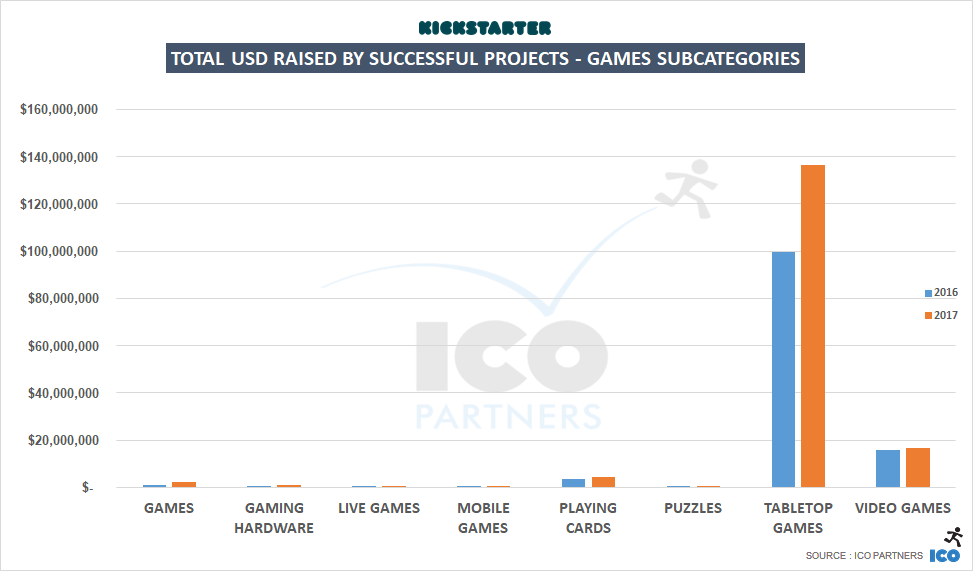

And of course, almost all of the growth in the total amount of money raised by Games projects is fed by the Tabletop Games subcategory.

And now, looking at the two big subcategories.

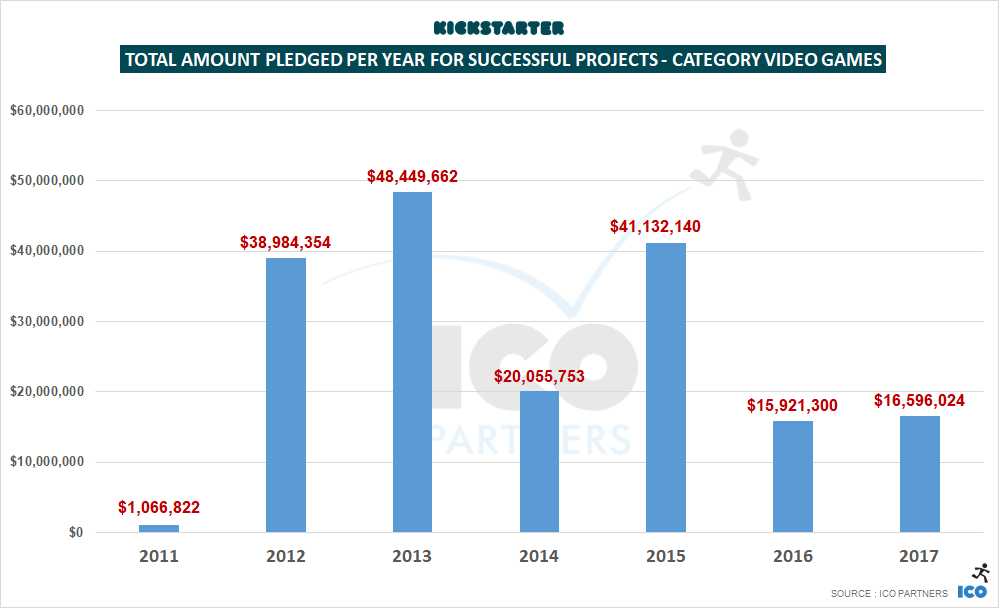

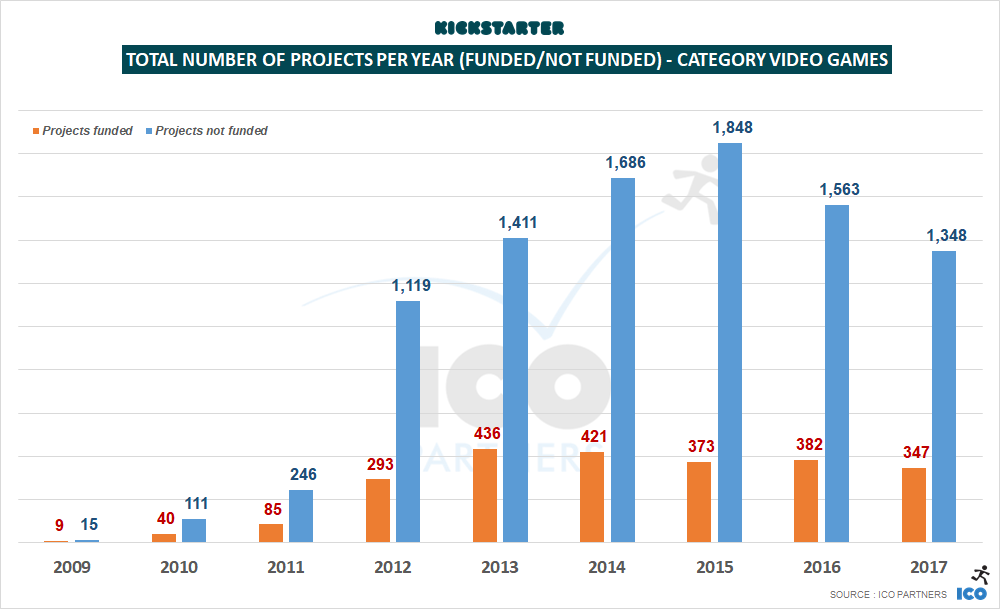

With slight growth in the total amount of money raised, and a slight decline in the total number of projects funded, 2017 doesn’t appear to be exceptional one way or another for video games on Kickstarter.

There are a few things worth noting, though:

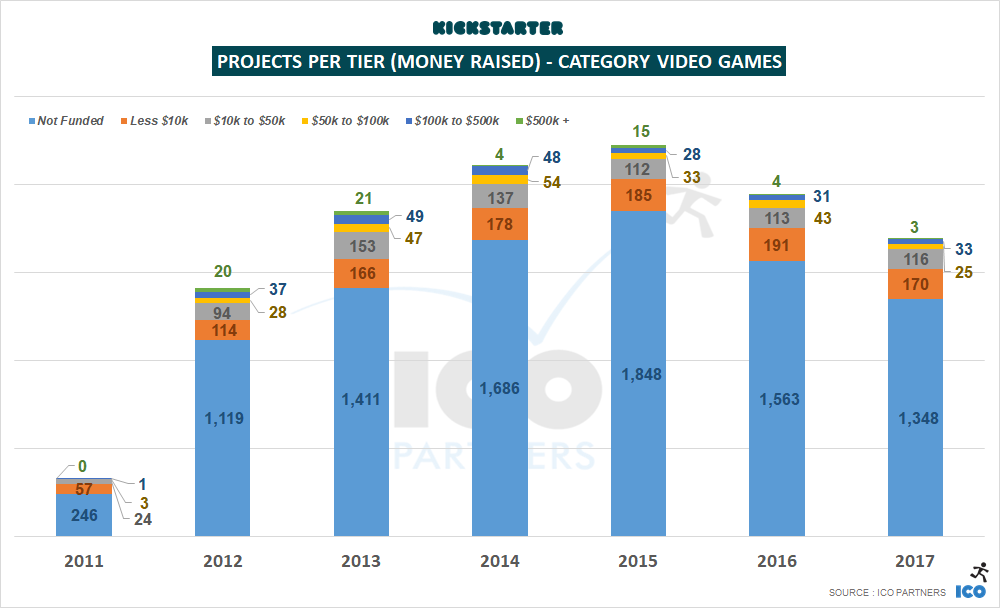

My theory for the decline of the smallest tier is that fewer creators are trying to crowdfund their projects, and it directly affects that range more than the others. Kickstarter doesn’t have the visibility it had in the media, and it doesn’t come up as often as it used to as a viable platform for small projects.

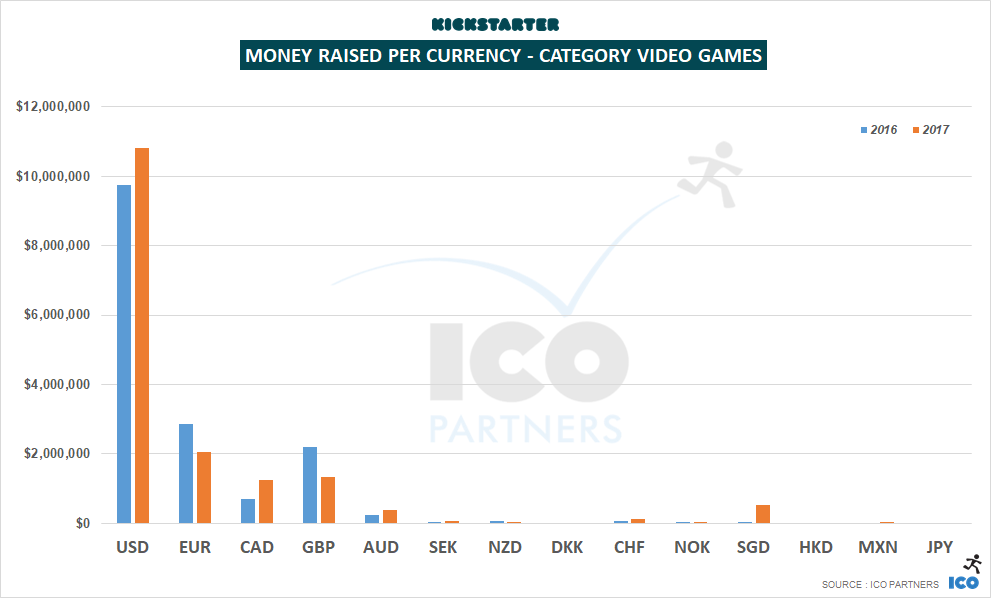

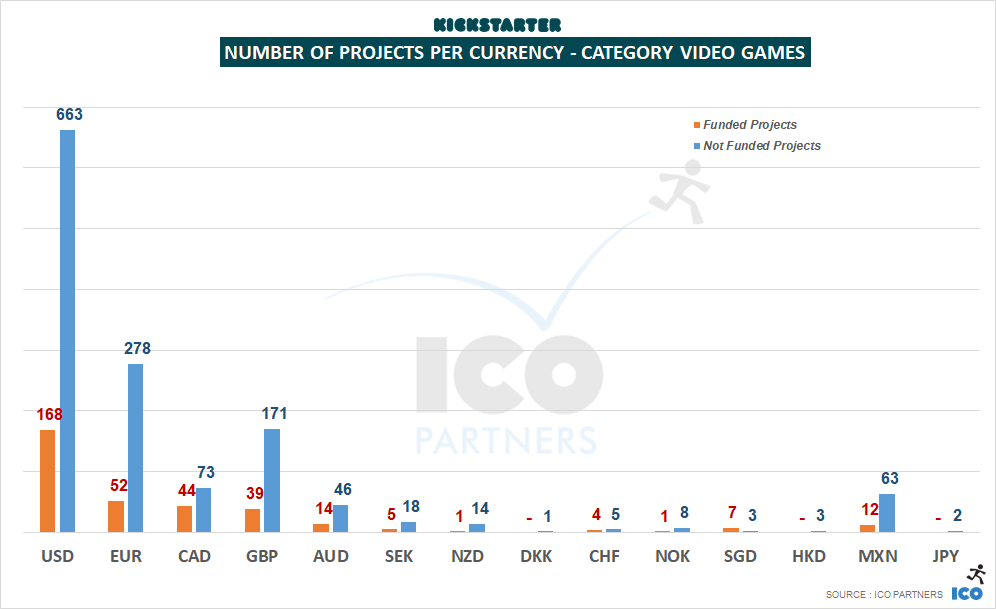

2017 was mostly a better year for video games projects launched in USD and CAD. A higher proportion of projects in those currencies got funded than those in EUR and GBP.

I found it interesting to see that 12 video games projects launched from Mexico got funded, even if that represents a small total amount in the end. Also notable is the absence of projects launched through the Japanese version of the portal, especially considering how some of the biggest crowdfunded video games of all time originate from there. Kickstarter’s September 2017 launch in Japan looks like a flop so far, and the video game category seems to be the best illustration of that.

These two graphs tells the most significant story of 2017’s figures.

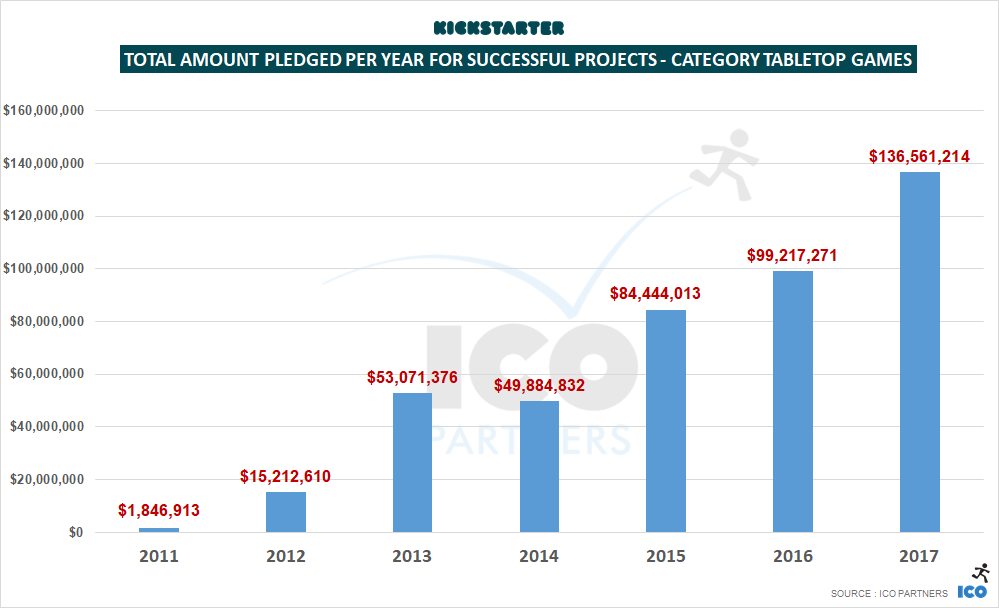

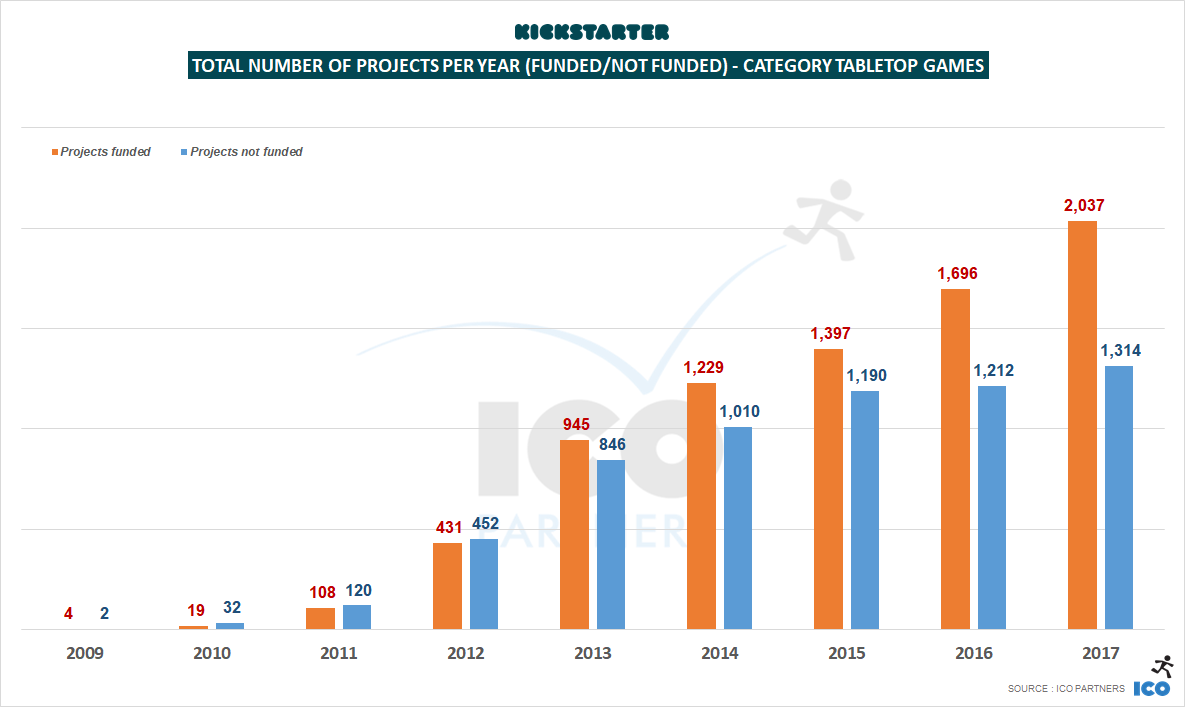

Tabletop Games have constantly grown over the past few years, both in terms of the total amount of money raised, and the number of projects funded. After a record year in 2016, the subcategory grew again, by +36% in 2017. The number of funded projects grew by +20%.

The growth invites questions, though. Will the subcategory stabilize? Will it crash? Can it keep growing?

There is no indication that its upward momentum will slow down anytime soon, even if record-breaking campaigns make it that much harder to keep up with the total amounts raised over a given year.

All the indicators for the subcategory are really healthy at the moment.

There has been growth across all tiers. This is, for me, a very important factor in determining how healthy the environment is, within this subcategory. If it were only good for the large, massive campaigns, it would not be a good sign; but having projects across all tiers growing shows that the ecosystem is not built upon a couple of metaphorical black swans, painting an inaccurate interpretation of the picture.

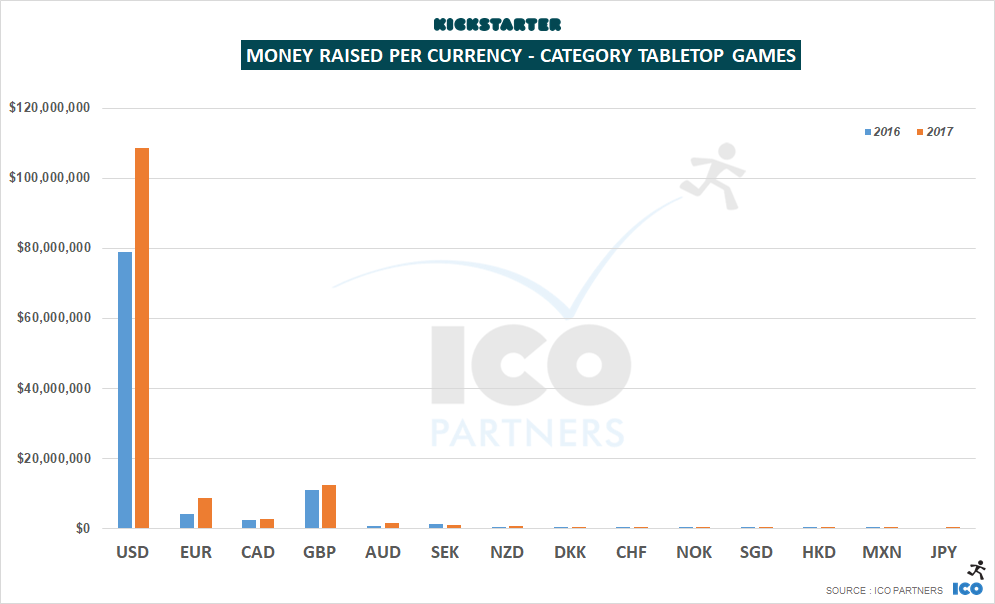

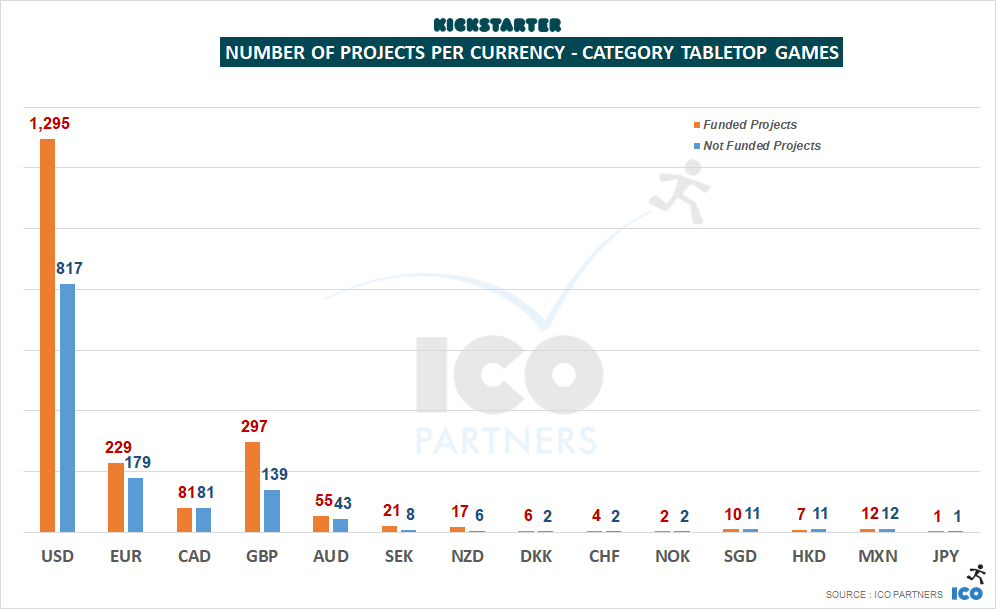

Projects across currencies are also finding success. Even if projects in USD represent the vast majority of the money raised and of the number of funded projects, projects in EUR and GBP are also healthy, representing more than 25% of the total funded projects.

This is especially interesting when you see campaigns that know that they will perform very well deciding to launch in USD, regardless of where they are based geographically. For example, 7th Continent, from a Paris-based company, launched their project in USD rather than in EUR.

Last week, at the PC Connects in London, I delivered a presentation about the state of crowdfunding in video games. One point I made was the fact that Early Access is a much bigger competitor to Kickstarter than any other platform. One reason for this is the fact that, over the last year, the optimal window to launch a crowdfunding campaign for a video game has moved closer and closer to its ultimate launch. This is how I illustrated this (you need to click the image to see the gif in action):

What is very interesting is that, for tabletop games, that window has moved as well. Projects need to be more and more polished to get funded, but physical production means that the optimal window cannot move any further to the right.

The other important difference between video games and tabletop games is the fact that, for the latter, Kickstarter is the end solution for distribution for most projects. Whereas for video games, the end solution is Steam – Kickstarter helps a bit, but you still need to go to Steam.

So if your game in Alpha or Beta has a lot of appeal and replayability already, the chances are that when it is good enough to be showed on Kickstarter, it is also good enough to launch in Early Access. It is a lot less hassle, as you only have to concern yourself with the end game distribution platform. Early Access, however, doesn’t provide a lot of the perks that crowdfunding does – building the community, the opportunity to test your publishing skills, and building awareness – but I suspect to many studios, this is secondary, or underestimated.

What is also true, and a strong trend, is that many video games projects on Kickstarter are games that, by their nature, don’t have a lot of replayability (like, say, Point-and-Click adventure games) or immediate accessibility and audience appeal, making Early Access a path they cannot take.

Like for all previous blog posts on the topic, we have been using the data on the Kickstarter pages themselves (with the help of Potion of Wit) and the collection method is not without its own issues. Please consider all of the numbers presented here as estimates.

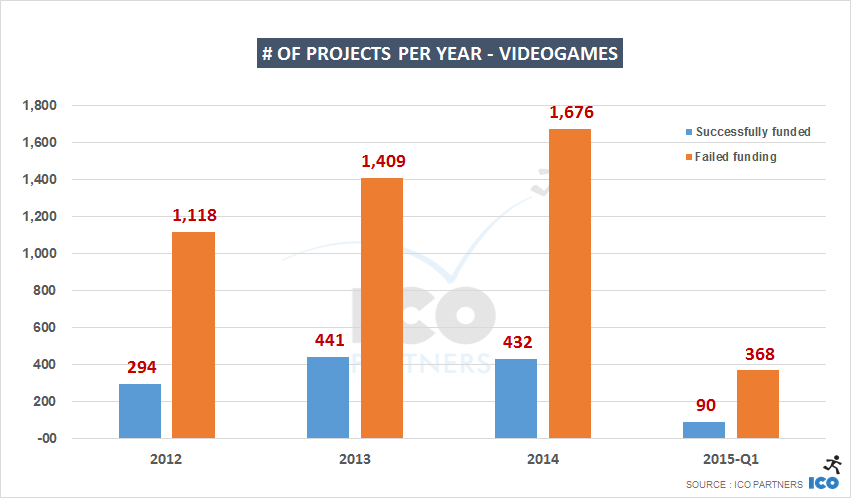

In my last blog post on Kickstarter, I explained how there was a significant drop in the amount of money that went to video games over the past year. Being 3 months in 2015, now seems like a good time to review how the year has started, and how it compares to last year’s trends.

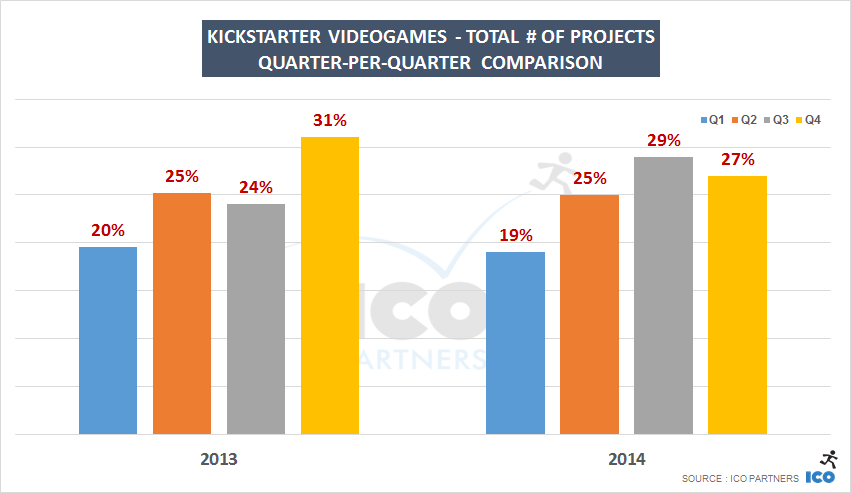

Before looking into 2015, I looked at Quarter-to-Quarter trends from the previous years – with the idea of providing more context when looking at the Q1 number for the current year in relation to patterns from previous years.

We are still in the early days of crowd funding, and I only have 2 years to look at properly: 2013 and 2014. Prior to 2012 the numbers are just too low, and 2012 numbers themselves are incredibly skewed by the fact that it took off after Q1.

Here is how I see the quarterly patterns:

Q1 is usually a quieter month. It’s after Christmas, and there are fewer projects overall. This means that we can expect it to accrue less funds.

Q2 is a very strong period. The best quarter in both years in terms of revenues and a strong proportion of funded projects (slightly higher ratio of funded projects as well, especially last year).

Q3 is the summer. Both years, it had the lowest quarter of money raised. I suspect big projects avoid to launch during the summer (wisely). But it also has the highest number of projects submitted (possibly that’s when hobbyist projects get launched as they have more time then?) – it doesn’t prevent them to get funded though.

Q4 is the pre-Xmas insane rush period for the game industry. Getting visibility then is extra hard, we can see it has a lower than average ratio of projects getting funded (true for both years). However, projects that get funded are well provided, this is the second highest quarter per money pledged. Probably helped by a few larger projects again.

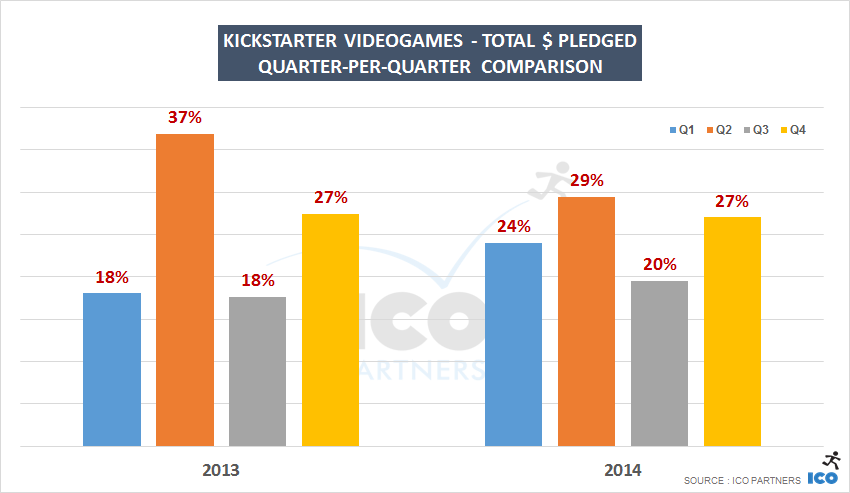

Purely in terms of money raised, 2015 is having a great start.

As shown above, Q1 is historically not the strongest quarter, and already more than $8.5 million has been pledged for videogame projects.

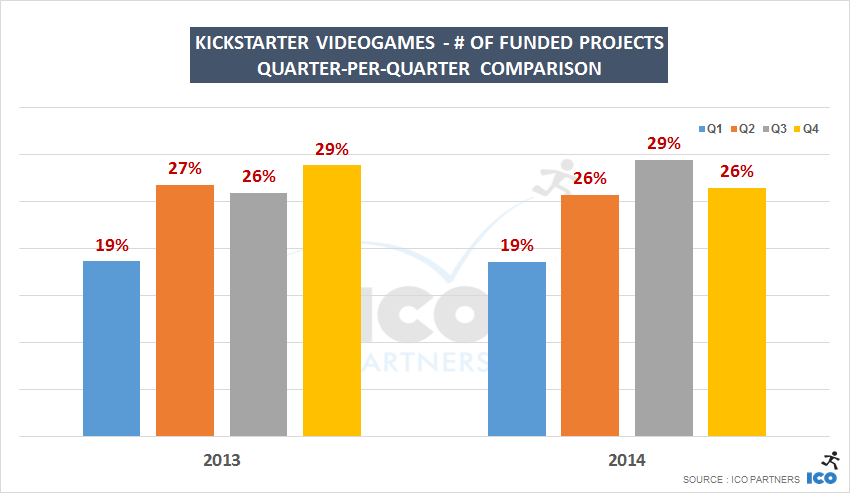

Looking at the number of projects though, it paints a slightly different picture. While money-wise, this year seems ahead of 2014, looking at the number of funded projects, we are in the same range as 2014 for the same quarter. And a similar ratio of projects getting funded (roughly 19.5% in both cases).

It means that Q1 2015 has had quite a few very well funded projects in proportion to Q1 2014 (and belying what was seen in Q1 2013 too).

So, I am left with an interesting question. Q1 2015 has started really well, from a money raised standpoint. But looking beyond those five very well funded projects, it seems like that quarter has not been performing on par with last year.

I used to tell everyone that big successes on Kickstarter were always helping the smaller projects, bringing attention to the platform and driving traffic to games that had more limited communication means. I am wondering if that effect has weakened somewhat (it was a very videogame specific effect, other categories didn’t see much of this) and if this is perhaps another part of the evolution of the crowd funding ecosystem for games. I think so, but it is still quite early to say.

And for what it’s worth, April is looking good so far.

Note on the methodology – Reminder on how data is gathered. It is automatically scrapped (thanks to a tool provided by Potion of Wit) from the publicly available data on Kickstarter.com. Because the website is evolving overtime, the scrapping methods is also changing. You may see discrepancies on old data we provided and data provided now. It mostly come from the evolving data scraping process.

Last year I did a general overview of Kickstarter across all categories for 2013 and now seems like a good time to go through a similar exercise for 2014.

I should start with the disclaimers though. In 2014, Kickstarter made a lot of changes to their website, changes that making data collection not as straightforward as before. I strongly suggest to look at this year’s numbers as estimates – all the trends they highlight are probably true but there might be a few inaccurate ones in there too, especially when the related data sample is rather small. Just keep it in mind.

You can find a complete, category per category, Slideshare presentation at the end of this post.

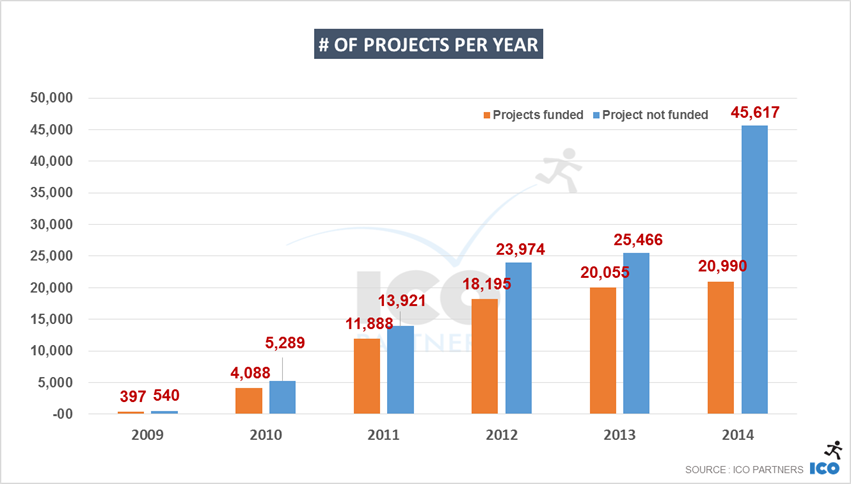

It all depends who you are I guess. If you are Kickstarter, 2014 was a good year. More money had been pledged on the platform than ever before.

While the growth in 2014 was not the leap observed in 2012 or 2013, it was still growth. Considering the remarkable successes of the two previous years, maintaining the trend is not a small feat and in that regard, we can probably consider this another winning year for Kickstarter.

For the creators on the platform, the outlook is a bit different.

On one hand, there has been more projects submitted to the platform than ever before: an impressive 46% increase from the previous year. When put side-by-side with the number of successfully funded projects, a 5% year-on-year increase, it tells a different story.

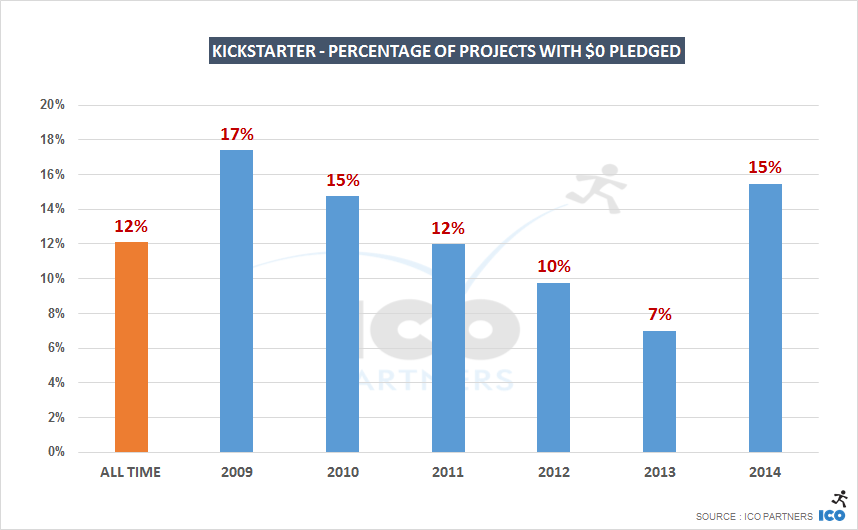

Kickstarter looks to have reached the point where the wider audience is fully aware of its existence. As a result it attracts more creators than ever, and we are probably seeing lower quality projects getting submitted in larger numbers.

This is very much illustrated by the percentage of projects that had $0 pledged towards them:

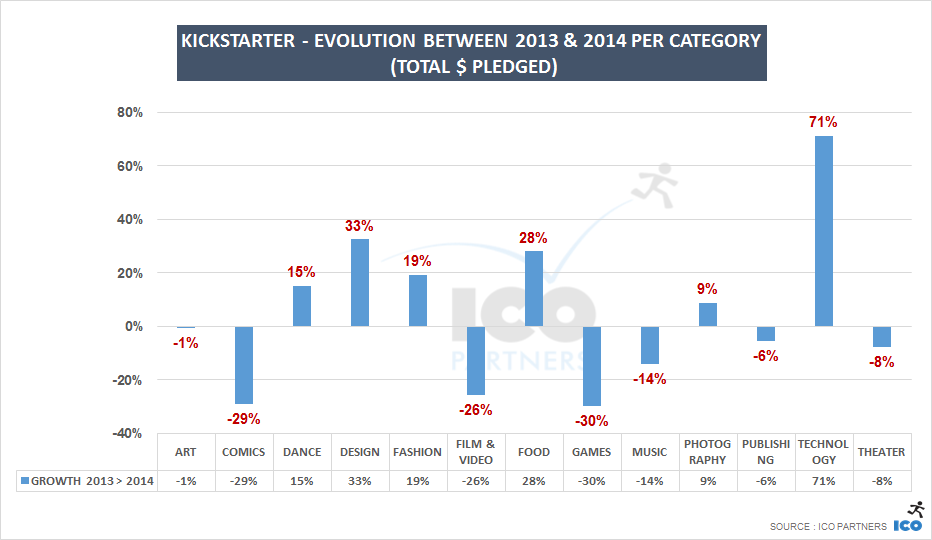

Back in September, I looked at how 2014 had been for Video Games on Kickstarter, and I did some projections showing that the numbers were going down from 2013. I won’t go in depth in any of the subcategories, but this is an interesting overview across all categories, showing their progress from 2013:

There has been a significant drop in the amount of money pledged for Comics, Films and Games on the platform in the past year. On the other hand, it was a fantastic year for Technology projects while Food and Design projects also performed very well.

But that’s only half of the story. As we have observed in the past, it is very easy for a few very large projects to weigh heavily on the overall amount of money pledged in one category.

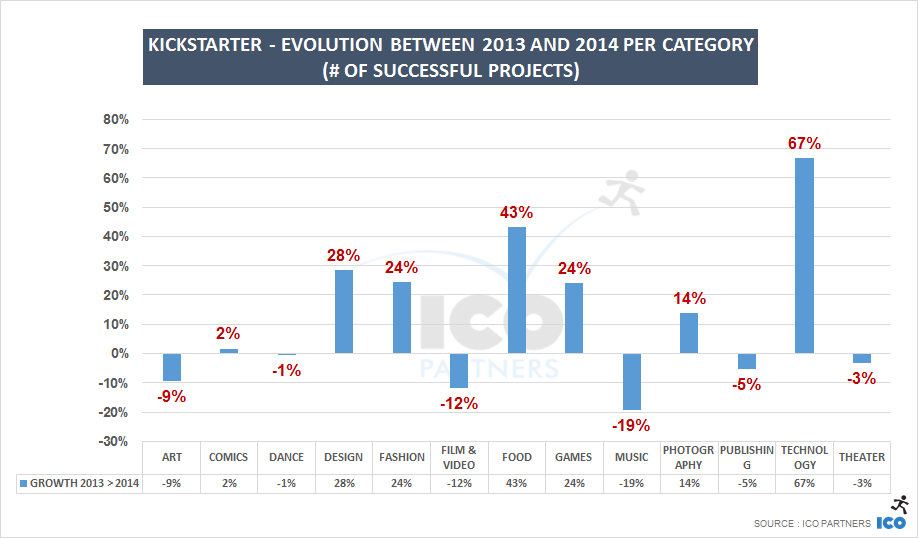

Year-on-year, looking purely at the number of funded projects, the only categories that saw a significant dip are Art, Music and Films. This helps illustrate that Games saw more projects getting funded than in 2013, despite gathering less money…

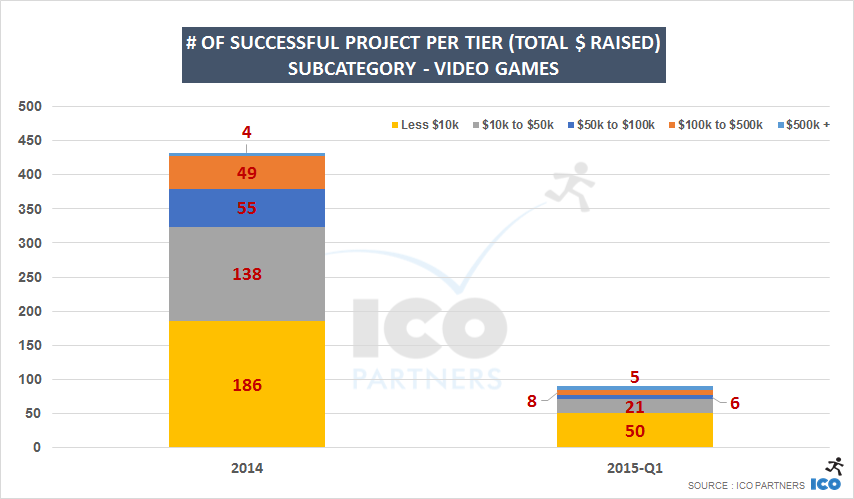

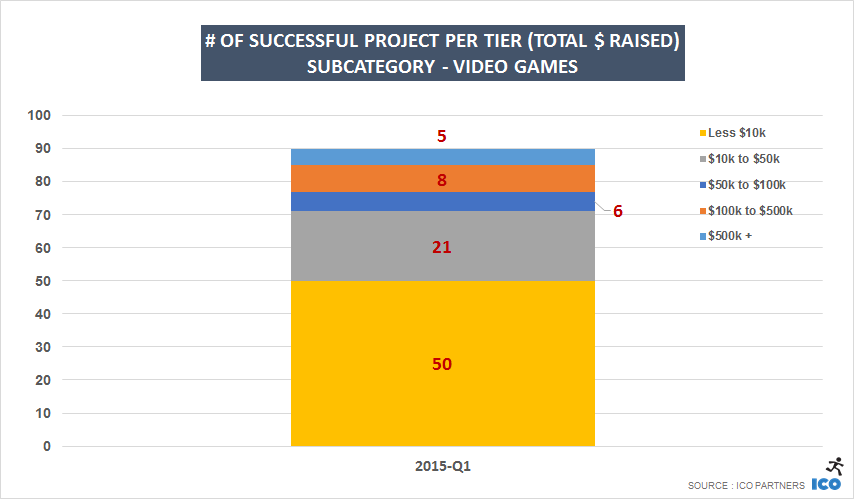

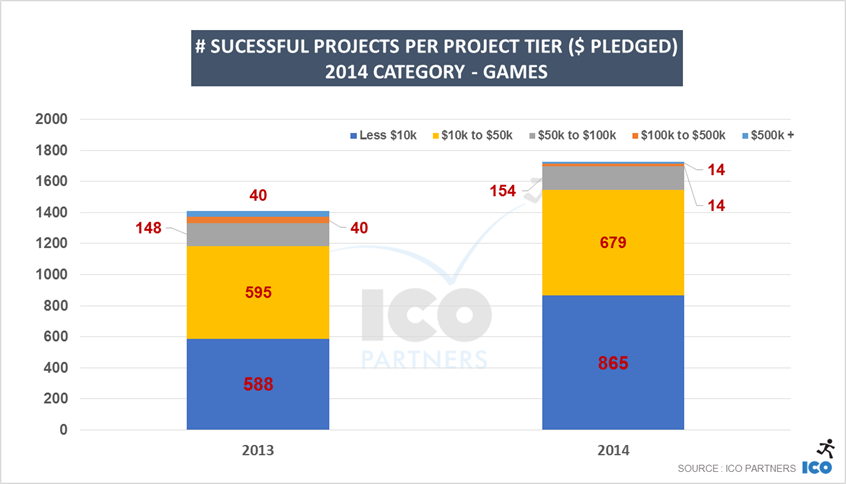

In a way, this means (in Games at least) that Kickstarter is getting more democratic and benefits more creators with projects with different scopes. And just to illustrate that thought, here is the Games category broken down per funding tier:

You can find this kind of break down for all categories in the Slideshare presentation…

All things considered though, we can say that it was a good year for picnic lovers.

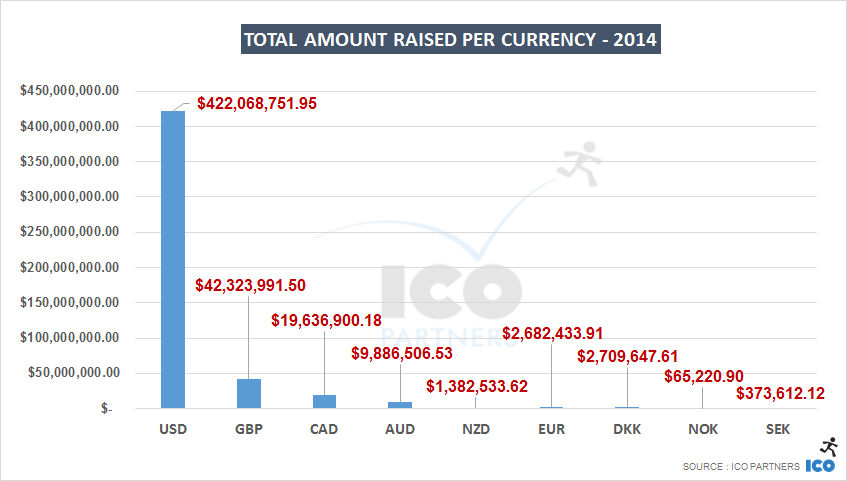

Kickstarter added another four currencies to its platform and opened projects to five new countries: Netherlands, Sweden, Denmark, Norway and Ireland.

The overall impact on the platform was not very significant:

The projects in GBP are still doing relatively well – along the same scope as last year.

It is worth noting that the Danish projects, the best funded of the newly added Scandinavian countries, did so through a few projects that raised more than $250 000 (including the very well performing Sitpack project). Anecdotally, 75% of those projects are Design projects. Denmark, right?.

Meanwhile, there hasn’t been a single EUR projects above the $250 000 line. Of course, large EUR countries such as France and Germany don’t have a direct access to Kickstarter and generally create their projects either through USD or GBP. It is worth noting however that the EUR integration didn’t seem to have much of an impact on Kickstarter’s development.

2015 will be interesting in regards to currency. One challenge that Kickstarter faced was that payments in USD were made through Amazon Payments, while all the other currencies were using an in-house solution. It meant that existing backers, with their card on record on Amazon, had to go through an extra step to be able to pledge money to a project not in USD. Now, all projects will share the same payment platform, regardless of currency. It should help the “exotic” currencies and remove a potential friction point in the process. On the other hand, no longer using Amazon Payments may have a negative impact too. Only time will tell in that respect.

UPDATE – I had a chat (very friendly) with Kickstarter and they highlighted that it was hardly fair to compare video games and tabletop games between 2013 and 2014 the way I did as they have added 5 new subcategories that further dilutes projects and increase the perceived dip for the two historical main subcategories. I have reviewed my numbers and added the new subcategories to the relevant pre-existing ones.

The slides represent this change now. To be clear, only the last slides were affected – the Video games and Tabletop Games sections.