Here is another Unabridged Comments (the fact I contributed to two articles in a short time frame kind of kicked me in doing this section). This time, it was MCV reaching out to me to discuss the unfortunate Kickstarter campaign for Fable Fortune. Like last time, I have fixed a few typos and rephrased some points I was making a bit.

- The piece is centred around Fable Fortune on Kickstarter

- The wider topic is why crowdfunding doesn’t really work for free-to-play titles

- The request came with a series of questions I have reproduced below to frame the discussion

Were you surprised [Fable Fortune campaign failed]?

Well – whenever you set rules, [like the “Free-To-Play games don’t get crowd funded” rule], you always have exceptions to prove them wrong. I would have thought the Fable brand to be strong enough to invalidate this one.

There were other things at play, [and] without going too much into it right now, one comment that came back a lot was on the fact that Fable is an Xbox franchise at its heart, and the campaign was addressing the PC audience first and the Xbox audience (in appearance) only after a certain very high stretch goal was reached.

How would you assess Fable Fortune’s Kickstarter campaign?

The Fable Fortune campaign was a surprise to me, and it didn’t unfold how I would have expected. The most important component to any campaign is to make sure you have an existing audience that you bring with you in the campaign, and Fable certainly has that. The franchise is incredibly strong. Another key component is to be able to show the game, and certainly Fable Fortune fit the bill there again. And while Free-to-Play games tend to have a very hard time getting funded, the few notable exceptions are all CCGs, which made me optimistic for Fable Fortune.

As far as campaigns go, I think Fable Fortune did a lot of things right, I suspect they failed (or more precisely they would have failed as they cancelled the campaign before the end and secured funding with a 3rd party) due to the change in the video landscape. With Hearthstone dominating the CCG genre at the moment, they don’t fill a niche that is in strong demand. They also diluted their message by announcing their Stretch Goals from the beginning, something that is really not recommended.

Do you think that free-to-play games can be successfully crowdfunded?

What challenges do you think free-to-play games face on Kickstarter?

The inherent promise of a Free-to-Play game is that you can try it for free, with no commitment, and as you play it, you may feel like putting your money into it. This is the opposite of what happens with a game that you crowdfund, where you build a promise that the game will be so interesting to you before you can play it, that you can safely put your money into it, months or years before you actually put your hands on it.

It makes funding a Free-to-Play game incredibly counter-intuitive. There are other principles at play too here. One of them is the fact that F2P games have offerings with a very large variance. You can spend a lot or you can spend a little. It might seem like it is the case for games funded on Kickstarter, where you can pledge at very different levels, but actually, the core experience offered is usually at one fixed price point (the price of the game), and everything else is additional perks on top of that core offering. This is not how most F2P games operate, and it makes it difficult for the potential backer to project how satisfying certain rewards will be.

And lastly, and it probably plays a role too, the profile of the most frequent backers for video games is certainly close to the profile of the players that are defiant of the F2P model: older, hardcore PC gamers.

What tips would you offer someone attempting to crowdfund a free-to-play game?

How would you assess the launch of Mighty No.9?

I’ve seen some people saying that [Mighty No. 9] may have damaged consumer faith in crowdfunded games. What are your thoughts on this?

I don’t believe in these kind of statements. There has been many badly managed campaigns in the past, some of them with more dire results than Mighty No.9 (Clang comes to mind), and the number of

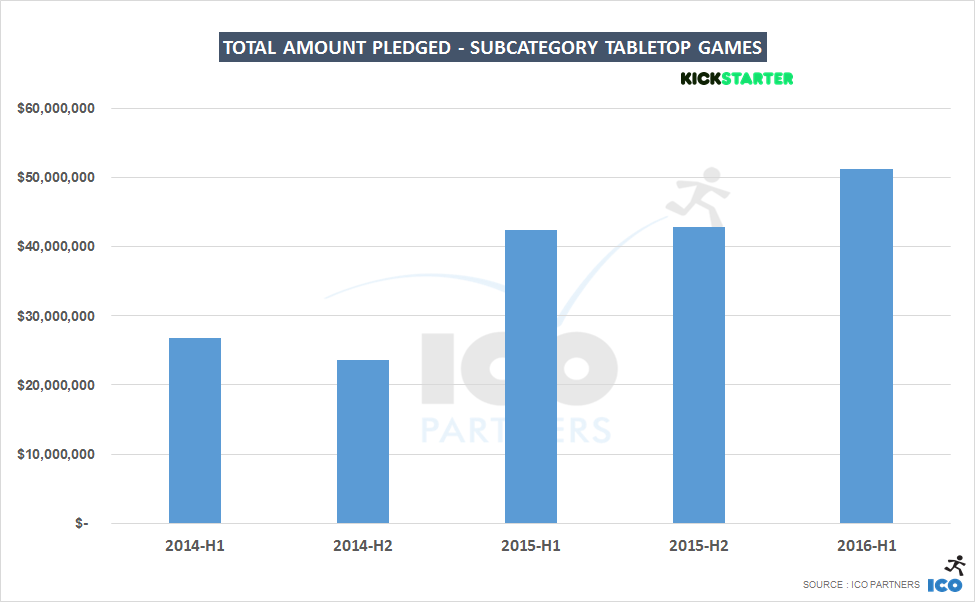

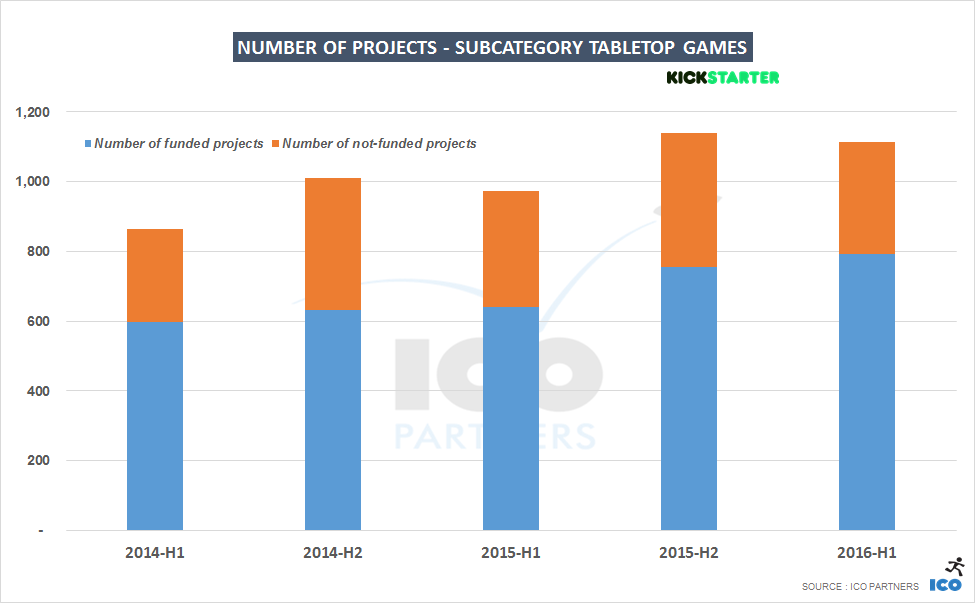

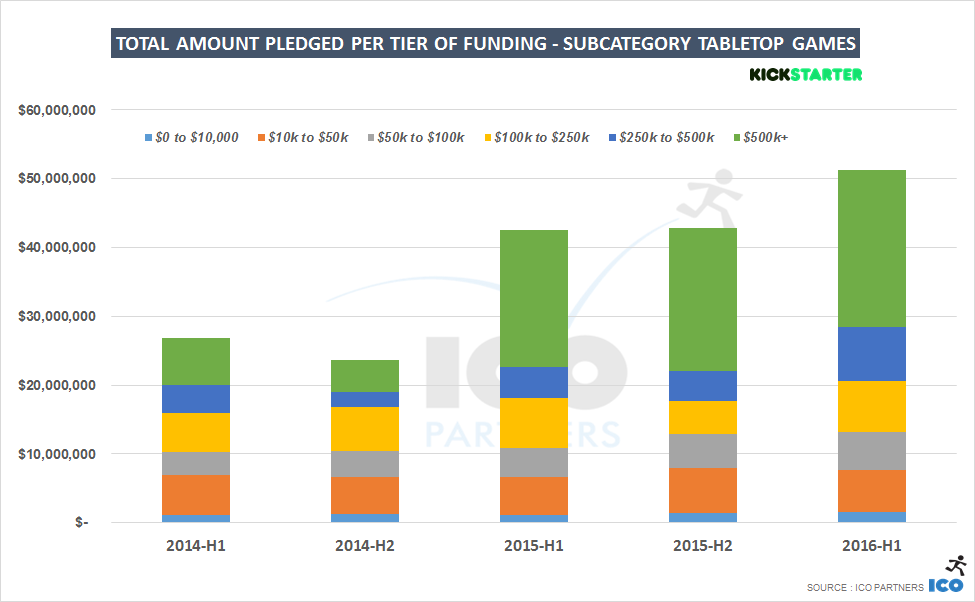

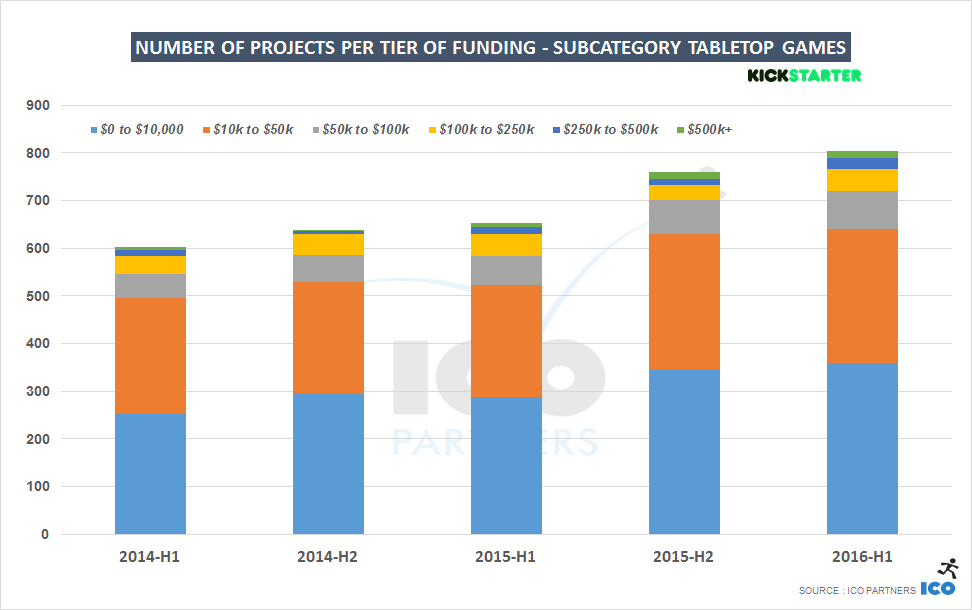

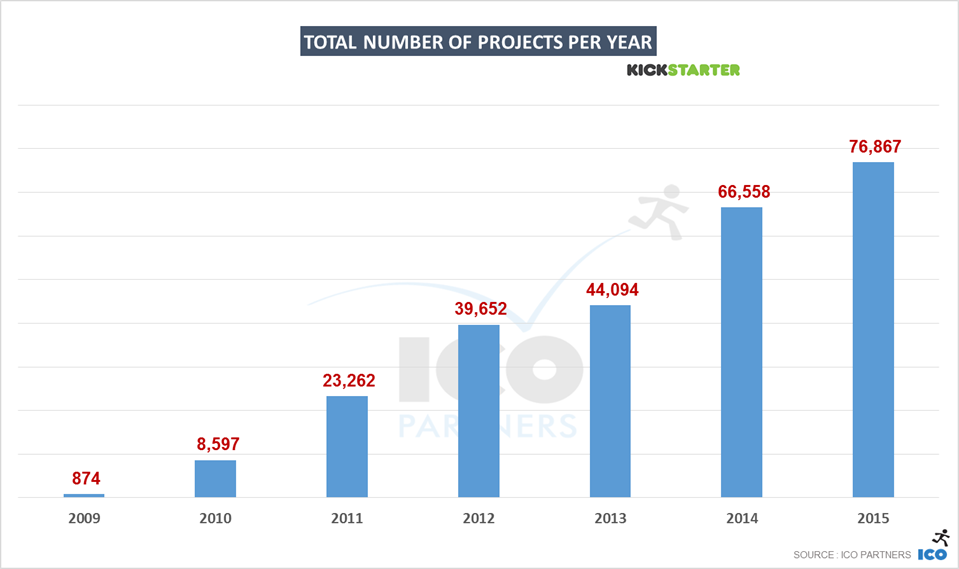

projects that get funded [every month] on Kickstarter is stable.

Anything else I haven’t touched upon that you feel is worth mentioning?