After writing my blog post on the 2013 numbers for games on Kickstarter, I felt like there was even more information to provide. While I am mostly following the crowd funding phenomenon in relation to games, the way we datamine Kickstarter means we have a lot of data for other categories too – sharing these is just a matter of taking the time to collate and make them presentable.

With Kickstarter hitting its first $1bn pledged this week, it appears to be perfect timing to provide more information to crowd funding enthusiasts. I hope you find it useful.

https://icopartners.com/newblog/wp-content/uploads/2014/03/kickstarter_header.png256710Thomas BIDAUXhttps://icopartners.com/newblog/wp-content/uploads/2020/04/CRUSHCREATIVE_ICO_BRANDING_LOGO_NavyWhite-01-e1586189748878.pngThomas BIDAUX2014-03-04 10:54:512016-12-23 19:48:18Kickstarter in 2013 across all categories

I am massively late in writing this post, and apologize to our blog readers as we didn’t have much time to blog in the last months. Like inpreviousyears, I will try to outline what I see as the biggest trends for online games for 2012.

Platforms

● Mobile and tablets : It’s a very easy prediction to make, and not very risky. We think iOS will remain a potent platform thanks to high ARPUs, and the explosion of Android-powered devices is finally constituting a huge addressable market in terms of volume, even if you consider the fact that the Kindle Fire doesn’t help much for the growth of that platform for games (limited hardware and more important, very tied to the Amazon ecosystem). Overall, the market for Android games in the short term is very dependent on Asian markets, which may be a challenge for Western developers. Some surveys tend to show a slowdown of apps developed for the platform as a result, which might make it an even more interesting market for those companies who know how to profit there. The total value estimates of mobile gaming for 2012 varies a lot, due to the uncertainty of estimating that growth, but most analysts put it between $3B and $11B . The PC segment will be gradually supplanted by smartphones and tablets. That should bode very well for connected games on these platforms. The average monthly playing time is around 15 hours for iOS and 9 for Android gamers, but companies like Spacetime Studios, with its Legends series (Pocket Legends, Space Legends, etc) are already at 25 hours. We are still far away from the average PC MMO player in terms of time spent (70/80 hours/months), but it is going up fast.

In terms of revenue, free apps with micro-payments are quickly becoming the standard there. ARPUs tend to be better than social games due to higher ARPPUs (ARPPUs above $10 are increasinglycommon), the average revenue per transaction being just under $15. Better news still, tablet games command even higher ARPUs, and even if the market is still small with an estimated worldwide installed base of 81M in 2011, it’s expected to grow to just under 400M in 2015.

● On those mobile platforms, we still hear a lot about HTML5 supplanting native apps. This might be increasingly true for the more casual end of the market (as companies like Zynga and Spil have started heading there), but as the higher value segment games become more complex, the “big client” apps (more than 50 Mb) will also progress. This is for instance where Glu Mobile is headed if you read their last investor relations document.

● Does it means that PC online games will die? Certainly not, but they are likely to focus on specific consumer segments : hardcore users on traditional PC genres (as was shown this year with the success of the MOBA genre, led by League of Legends, and action/shooter games such as World of Tanks or Combat Arms), browser-based games targeted at office gaming, maybe kids and teens who don’t own portable devices. The “middle core” is likely to be squeezed out, along with the categories where the competition is making success more difficult such as RPGs(see genres).

● Social gaming seems relatively constrained on Facebook, as acquisition costs keep rising. According to recent figures from Atul Bagga, a ThinkEquity Analyst, Zynga’s cost per acquisition increased fivefold in 2 years, from $0.3 in 2010 to $1.5 now. It gives more weight to the big publishers there as they can rely on cross-promotion better than others, and also pushes everyone to focus on better retention and monetization. That is probably good news for companies such as Kabam and Kixeye. Retention remains a problem and sequels don’t work there, so we can also expect better endgames. Also, more social gaming companies in 2012 should try to push distribution to other platforms than Facebook where their margins won’t be so squeezed, whereas on their own platforms (like Zynga Direct), competitor SNS or via embed on every possible platform (a strategy that so far was pretty successful for Goodgame Studios, for instance).

● We also hear a lot about connected TVs, but it seems to us that it won’t be such a big trend for 2012. Samsung announced it sold 2 million devices in June last year, and it is looking to sell 25 million in 2012. However, this will depend on the replacement rate for the household television market, and we would bet on it to be very tied to the overall economic situation, and at least in Europe it should stay gloomy. It is also likely that the big players on this space will be those already present on the mobile space, but they will have to solve other challenges such as gameplay input.

● Cloud gaming seems still promising on paper but we also doubt it will become really huge in 2012. OnLive is apparently in the range of 2.5 million subscribers and is likely to have its international growth limited to some markets due to infrastructure issues. Gaikai has reached 10 million MAU but will probably be limited in its growth due to their business model : even if they do reach 100m MAU as they target in 2012, it will still remain very limited to limited-time demos of mostly product-based games.

● We still believe that more industry players will try to implement some forms of cross platform features and gameplay during 2012, particularly in the interactions between web/social/mobile . However, few companies are well positioned so far for doing so, as the successful tactics are very specific to each platform. Business models and business topics

● By now we can already consider that the “free to play with micro-payments” business model has largely won, with the exception of a few cases where actively limiting ARPPU makes sense , mainly in games for kids (where the parents might object). Even in that case, alternate solutions such as wallets or spending limits might work better. Does that mean that subscriptions will die completely? Once again, probably not, as they may as well mutate. In many micro-payment free to play games, there is a “subscription-like” option where bundles of services or special are offered at fixed price points. Also, in the few remaining subscription-only games, there are a couple of extra services that are generally paid in addition to the subscription fee (although generally they are very one-time in nature, as opposed to consumable-based cash shop item majority.). The main problem with subscriptions are the cap on revenues and the barrier to entry. If those are removed, subscriptions can become attractive again.

● Player acquisition is set to continue being a major headache. On the web, iQU published recently stats that showed a 152% increase in CPL in UK, US, FR and DE territories. On mobile, the cost to acquire a loyal users for an app (opens it 3 times or more) was $1.81 in December 2011. On social, as stated above, it has increased 500% in 2 years for some actors. As this seriously eats into industry margins, it will probably lead to the demise of the less efficient players (expect some more concentration in 2012, particularly in the most mature segments such as client-based and browser-based MMOs), the rise of big traffic purveyors (eg increased partnerships with old-media and web portals), and increase the incentives for companies to capture underserved segments, for instance demographic (eg male 30+ is coveted by companies such as Supercell and Cliffhanger Production), geographic (Eastern Europe, Turkey, Indonesia, Brazil…). At Browser Games Forum in November last year, it was asked when publishers will start directly paying players to try their games (like the poker industry does). I don’t think this will directly happen in 2012, as CPAs are not that high to be a sufficient motivation for players, but maybe we’ll see some meta-rewards companies getting there. For platforms with very limited acquisition options (like mobile), we should see more dirty tactics (or cleaner ones in terms of incentivisation) to game the system on the one hand, and more reliance on other mechanisms such as virality, curation, branding, etc. to escape the system on the other hand. Mobile could also benefit from IRL discovery mechanisms : outdoor advertising, “tupperware parties” etc.

● The resulting focus on retention and monetization will lead to a better command of analytics by all actors, and probably to the development of better reacquisition channels and CRM. The past year has seen a lot of CRM tactics employed by the social games industry, mainly through email. The mobile segment is so far bad at retention : churn for all apps was estimated at 62% in the first month by Flurry. Once again, tactics such as community management, events, CRM, tournaments, branding will develop over time to boost retention rates. Tools and UI to help manage existing apps should also improve. In terms of gameplay, that should bring better endgames and more attention to long-term gameplay (whereas the recent free to play move focused a lot on the initial experience only).

● Is that the beginning of the return of third-party publishers? So far, it seems that it’s still difficult to operate online games from another developer. Recent PC successful companies like Riot Games or Wargaming chose to operate the games themselves in all territories. Most browser-based successes such as Farmerama have also been developed internally. So far, third party games published by the likes of Jagex and Innogames have not materialised the same success as their forbearers. In the case of existing publishers with different entities, the trend has been to decentralise completely the activities and let the studio run all the operations (as Bluebyte did for Ubisoft, or EAsy and Playfish are doing at EA.). In social games, there has been a lot of announcements for third party publishing (Playdom/SpryFox, RockYou third party deals, 6waves/Lolapps) but there hasn’t been stories of hugely successful 3rd party products (also, probably because it’s still easier to buy the company or clone the game.). For mobile, things are slightly different as there aren’t so many truly online and connected mobile games. And for mobile and social games it still makes more sense for a publisher to quickly buy the developer than to publish them as third party. We’ll see, but I wouldn’t bet on a return of publishers so far. What I’m ready to bet on, is an increased reliance on third party tools and services for online games companies.

● Speaking of those, we should see yet more concentration on services where the differentiation is low and the margins are getting thinner, mainly traffic acquisition and payments. Both industries should see concentration (or further concentration in the case of payments) and differentiation strategies.

Genres of games

● Old-school PC MMOs should stagnate or decline, as there aren’t so many pharaonic huge client based games in the pipeline and retention rates should drop for the most recent ones due to the lack of innovation. Most of those not released yet are coming from Asia and are also likely to run into 3rd party publishing issues.

● More action : it’s another trend we see continuing: the traditional point’n’click MMO gameplay is replaced by alternatives coming from different game genres – from action-RPG to fighting game to FPS . In a parallel course, most traditional genres are starting to include MMO elements. This is also true for mobile games, similarly to Spacetime Studios’ Legends series they should become more real-time, while incorporating asynchronous elements.

● More crossover declinations of successful genres : eg Infernum’s Minecraft/FPS combination, MOBA/RTS mashups like Tindalos’ Stellar Impact, etc. Most of the innovation will come from indie studios. The downside is that those gameplay mechanics will be copied quickly if they prove successful.

Please don’t hesitate to discuss and give your opinion in the comments!

https://icopartners.com/newblog/wp-content/uploads/2020/04/CRUSHCREATIVE_ICO_BRANDING_LOGO_NavyWhite-01-e1586189748878.png00Dianehttps://icopartners.com/newblog/wp-content/uploads/2020/04/CRUSHCREATIVE_ICO_BRANDING_LOGO_NavyWhite-01-e1586189748878.pngDiane2014-02-20 10:40:002016-11-28 06:13:34Online games trends in 2012

Virtual Worlds Management has posted its update on Youth Virtual World sector. If it seems to you that the sector is crowded, it’s probably because it is : they numbered 200+ of them. Read more

https://icopartners.com/newblog/wp-content/uploads/2020/04/CRUSHCREATIVE_ICO_BRANDING_LOGO_NavyWhite-01-e1586189748878.png00Thomas BIDAUXhttps://icopartners.com/newblog/wp-content/uploads/2020/04/CRUSHCREATIVE_ICO_BRANDING_LOGO_NavyWhite-01-e1586189748878.pngThomas BIDAUX2014-01-17 20:48:352015-02-20 11:00:15200+ virtual worlds for kids live or in development

With a new year starting, it is time for two customary types of blog posts: retrospectives and new year wishes. Here, I have decided to combine them both for you.

Considering how much time I have spent looking at and talking about Kickstarter data, it would be a shame to miss the opportunity to join the crowd of analysts of the platform in giving my own take of the past year – with my usual focus on games in general, video games specifically.

[reminder – for the purpose of our data analysis, we re-qualified the Ouya as a Technology project]

2013 and Kickstarter

In 2013, there has been $477m pledged on Kickstarter, across close to 45,000 projects. About 20,000 projects got funded this way.

Games represent the largest category on the platform, in front of Films, and by a large margin.

Video games in 2012 and 2013

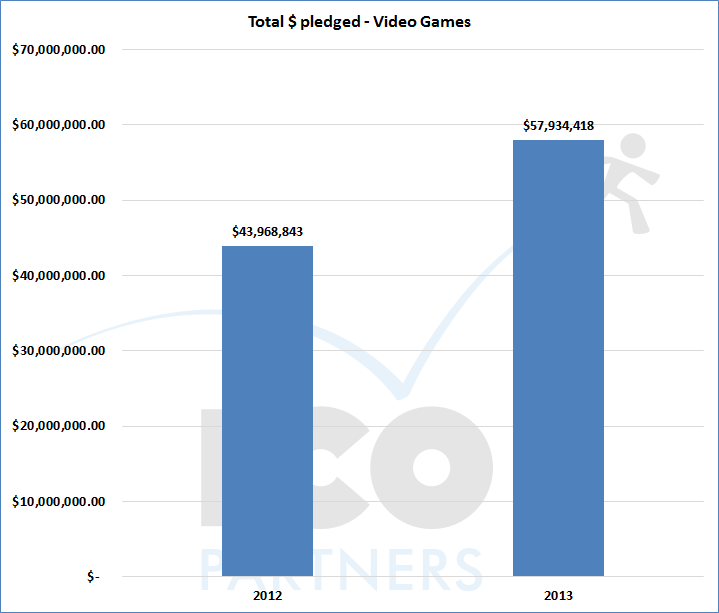

2012 was a remarkable year – it saw the Double Fine Adventure project put Kickstarter on the map for independent video game developers all over the world and the number of video game projects explode on the platform. From $1.2m pledged in 2011, Kickstarter went to close to $44m in 2012.

Throughout that year, a number of projects reached very impressive numbers for their funding and 2012 can be seen as Kickstarter Year One for video games for sure.

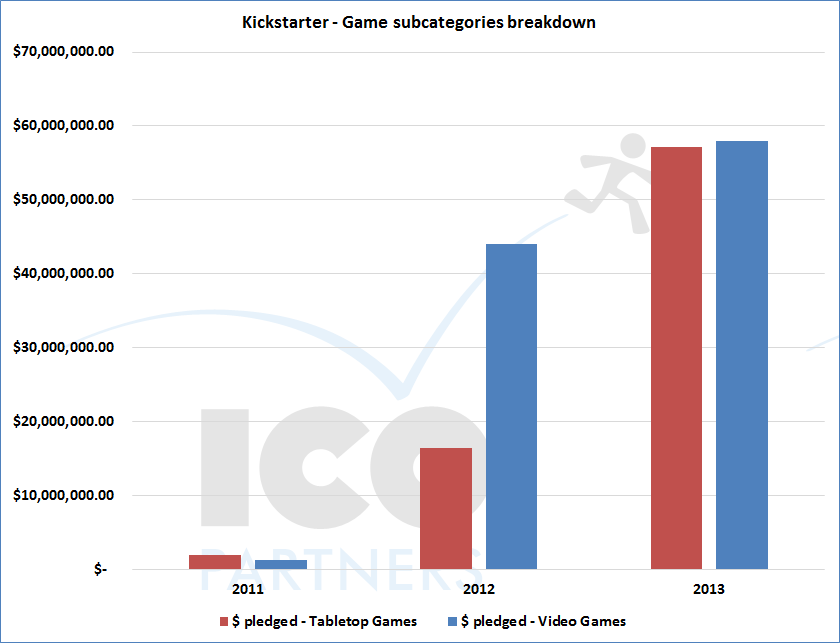

So what about 2013? We saw that games as a category did very well, but you have to account for the fact that the category itself accounts for both video games and tabletop games projects.

Yep, that’s right. Tabletop games represent almost half of the money that was pledged for games on Kickstarter in 2013. Being a board gamer, it makes me incredibly happy. But more on this later, I will keep looking at video games for now.

2013 was to be a key moment – would the trend of growth continue and was it going to be steady? Or was there to be a collapse as the first large projects got delivered and a certain fatigue for crowd funding crept in?

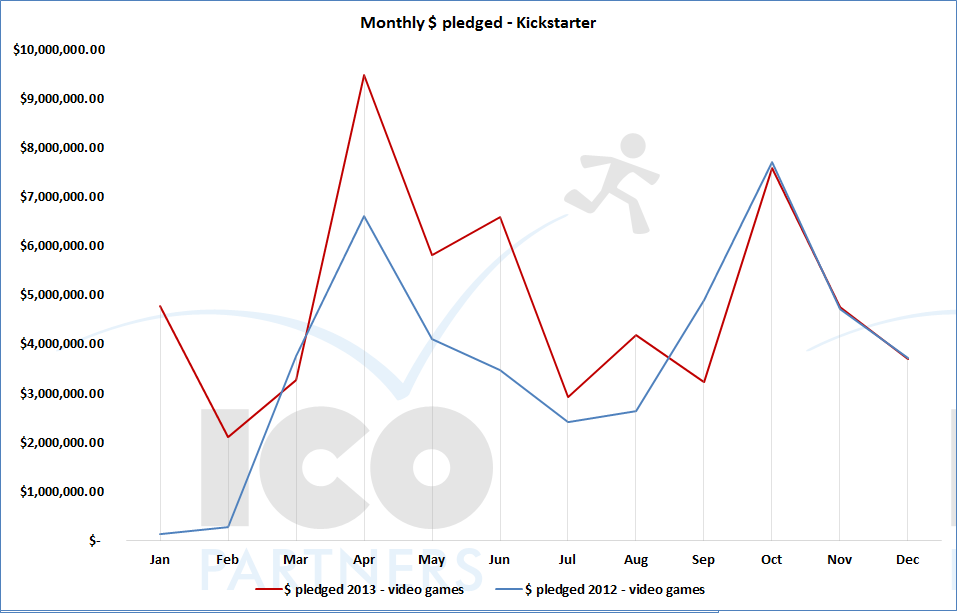

Purely looking at the total of money pledged for video games projects, it is obvious that 2013 was a better year than 2012. About 30% better. But such a snapshot can be a bit misleading – 2012 had a slow start with the Double Fine Adventure explosion happening after February.

Looking at 2012 and 2013 month-by-month is interesting: you see that the end of 2012 and the end 2013 had almost the exact same volume of money being pledged. The difference between the two years mostly happens in the first half. It is not a big stretch to imagine that a plateau has been reached and that variances are created by the “hits” (post $500k projects). And, to be honest, I am less interested in those large project performance than I am by the potential of the platform for small projects.

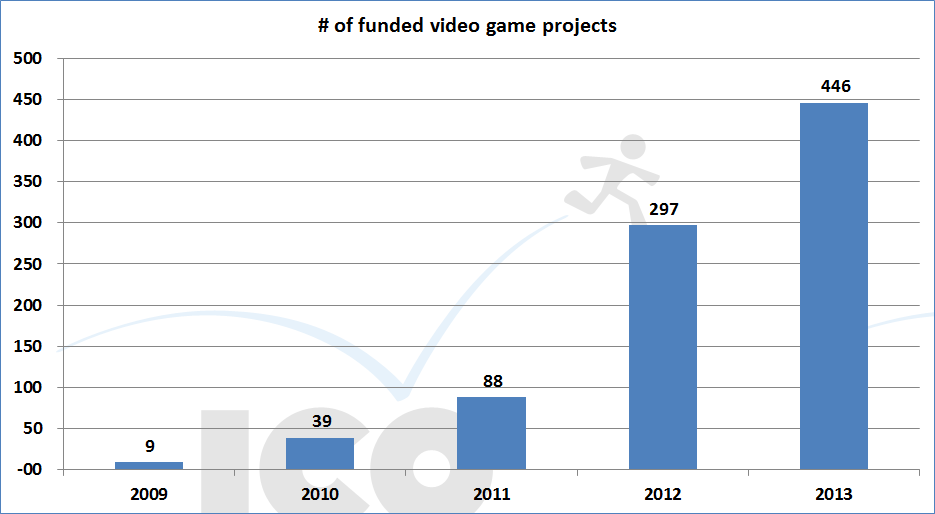

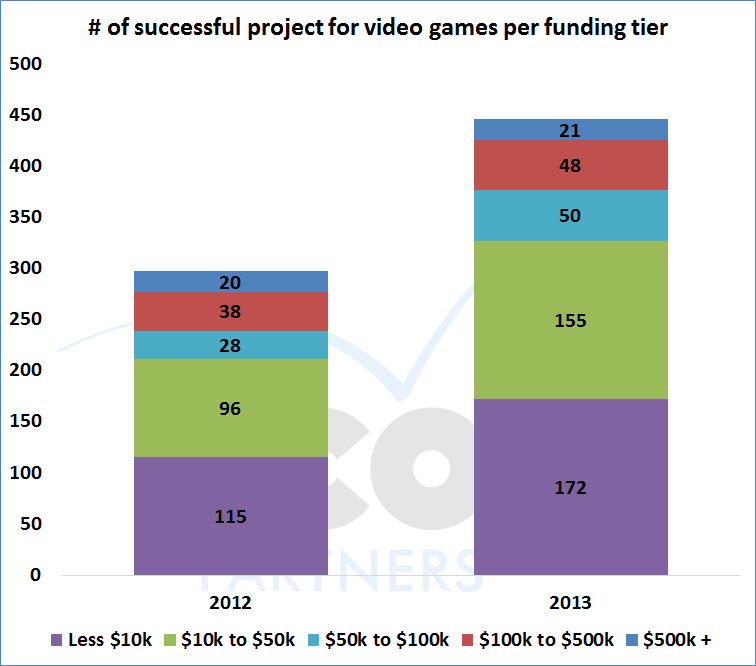

For Kickstarter to get a foothold in the game industry as a source of funding of interesting projects, we need to see projects of all kinds being successful on the platform.

It is reassuring to see that a similar number of projects funded in 2013 compared to 2012, and a much better indicator to see if the model is sustainable.

The following graph shows the number of successful projects per “funding tier”. The funding tiers are based on the amount of money the project raised and were empirically set by me. I think they represent meaningful tiers for independent games budgets.

So basically, between 2012 and 2013, the number of $500k projects is essentially the same (around 20), but there has been 25% more projects raising between $100k and $500k. 80% more projects raising between $50k and $100k, 60% more projects raising between $10k and $50k and 50% more projects raising less than $10k.

And to me, this looks like good news overall. It shows a wider selection of projects can get funded via Kickstarter, and not just the very cheap or the very famous. I would be ok for 2014 to see fewer shiny, large projects if that would mean a larger number of projects found a way to get funded. I think this evolution stems from the development of a community of video game enthusiasts embracing the crowd funding principles. A growth from the bottom up sounds a lot healthier overall.

Some numbers

Graphs are nice, but you probably want to have some direct numbers from all this. Worry not, I am very happy to provide the ones we have (all for video games projects):

2013

Number of pledges made

1,129,522

Number of projects submitted

1,851

Number of projects funded

446

Number of projects that failed getting funded

1,405

$ pledged to video game projects

$ 57,934,417.74

Success ratio

24.1%

In 2013, Kickstarter expanded its platform to new countries: Canada, Australia and New Zealand. And we also now have a full year with the British platform. I explained my thoughts on some reasons why this dones’t necessarily mean much, but if you want to know the repartition between the currencies, here it is:

Kickstarter platform

$ pledged – Video Games

USD

$ 50,370,976.75

GBP

$ 5,910,926.00

CAD

$ 1,336,856.70

AUD

$ 287,084.96

NZD

$ 28,573.33

(Currencies converted into USD equivalent)

Tabletop games and video games

So, tabletop games got huge this year on Kickstarter:

It personally makes me very happy (and I did contribute actively to that category myself) as I love board games, but it also makes me wonder what video game projects creators could learn from tabletop game projects.

The main problems their funding is to solve are fundamentally different. Video games have a high, fixed cost (the game development) and board games have a high, flexible cost (production and shipping of those games). That’s why the crowd funding works so well for board game as they can scale their main cost based on their popularity, a luxury video games don’t have. On the other side, video games have a lot of flexibility in the way they can deliver their projects and the way they can spread their development process over time – Double Fine and Revolution both deciding to deliver their games in two parts is clearly playing to that advantage.

But I digress as I think there is a lesson to learn from the success of board games (just FYI, the success ratio of tabletop game projects in 2013 was 53% compared to the 24% of video games):

Aim for the smallest amount that guarantees you can deliver your project.

Kickstarter is a platform that is perfect for projects that don’t aim for the moon, but promise a quality experience for the amount they ask for. I get to review a lot of projects on a regular basis from video games studios since I have started blogging about the crowdfunding of games – the vast majority of them are simply too ambitious and too expensive when considering the studio’s track record and its reputation. This is not the only point of failure there is, but this does seems to be the most common.

So, if I have a wish for games on Kickstarter for 2014, it might be “be more humble, be more successful”.

Special thanks to Potion of Wit for their help in the data-mining process.

And to end this note

Oh, and I didn’t forget that I promised this blog to cover two purposes: have a wonderful new year, we wish you and your families all the best for 2014!

https://icopartners.com/newblog/wp-content/uploads/2014/03/kickstarter_header.png256710Thomas BIDAUXhttps://icopartners.com/newblog/wp-content/uploads/2020/04/CRUSHCREATIVE_ICO_BRANDING_LOGO_NavyWhite-01-e1586189748878.pngThomas BIDAUX2014-01-10 10:48:182015-01-30 08:35:052013 for games on Kickstarter

Anyone who met us at gamescom this year know that we have been working on two new reports on the game industry and we are very pleased to announce that our market research on the Turkish video game market is now available to everyone on our website.

It was a very productive collaboration with Smart N Digital Marketing whose insight in the market was essential as we prepared the report. We also received a lot of support from local actors who answered a lot of questions and shared their insight with us.

You can find details on the report content over here.

We made an infographic to illustrate some key data on the market:

https://icopartners.com/newblog/wp-content/uploads/2014/07/turkish-report_blog.png256710Thomas BIDAUXhttps://icopartners.com/newblog/wp-content/uploads/2020/04/CRUSHCREATIVE_ICO_BRANDING_LOGO_NavyWhite-01-e1586189748878.pngThomas BIDAUX2013-11-01 10:11:132014-09-23 10:58:23New report: Video Games in Turkey Market Research

It has been some time since I last checked on the progress of Kickstarter in the UK for the blog. With Kickstarterlaunching in Canada next week, it seems like an excellent time to look at the performance of the GBP projects again. I have pulled some data (from early July) and tried to get a feel for the current trend.

I like to look at things and keep them at a comparable level – all the numbers you will see here are only for the first half of 2013. As I explained in the very first blog poston this topic, the early months were not very representative of the success of the platform in the UK, so being able to look at the 2013 data should be much more telling.

The fact we now have much more complete data, I can also look at things such as success ratio and other categories of projects. It also means it is a bit of a bigger picture. To make the whole thing easier to read, I have put the larger part of the findings in a Slideshare presentation. I recommend viewing it full screen:

My concluding thoughts from looking at the current state of the two ecosystems:

– The two ecosystems are not on equal footing. The UK Kickstarter seems to suffer from being in a currency not as widely understood as USD (as this is the biggest difference from the US ecosystem) as well as from the difference of payment systems (Amazon payment in the US, Kickstarter’s own system in the UK).

– Kickstarter has grown from adding the UK ecosystem. It is quite clear as most of the successful UK projects are rather small (compared to their US counterpart), they would not have been able to go through the US ecosystem in the first place (it requires too much energy/investment for a small company), and they add up to the growth of Kickstarter overall. That growth is just significantly smaller than the one observed in the US, but it is commendable.

– It also seems that the US creators are better at understanding their capacity to raise money from the crowd and at managing their campaigns. The quite low success ratio of GBP projects compared to USD projects cannot be solely blamed on the difference between the two ecosystems. I think that, in general, GBP are overshooting for their goal – it could be that they are more honest about the amount that they need to build their project, the cost of development is more important in the UK, the Brits are not as good at getting attention to their projects, or a combination of these. I have seen many UK projects that had a fairly high goal and very few channels where to recruit backers. Now, me being based in the UK, I tend to talk to more UK creators and this could be anecdotal.

– The UK ecosystem won’t grow significantly until the option to show the pledge rewards in another currency is added or a few large projects make the leap of faith (and there is proof that both ecosystems can efficiently support large projects). Anyone looking a bit closer to the behavior of the ecosystems could conclude that any large project would be better off going on US Kickstarter. The difficulty to get into the ecosystem (set-up as US entity, set-up an Amazon account) can be overcome for the right project, with the right size, and it then become a self fulfilling prophecy: all the big projects are on the USD ecosystem, ergo, if you have a large project you should put it there. You have a few exceptions (successful Australian projects on the GBP ecosystem), but you would need more of those to counteract the current trend. Ideally, you want the project creators to go to the ecosystem that is the easiest for them and there is a noticeable gap at the moment between the two ecosystems.

The addition of Canadian projects will make the platform grow further, it will be interesting to see how projects perform there compared to the UK projects.

In the meantime, I will hopefully be able to dedicate more time to build more comprehensive graph representation of those trends.

https://icopartners.com/newblog/wp-content/uploads/2013/09/kickstarter-uk_ico.png256710Thomas BIDAUXhttps://icopartners.com/newblog/wp-content/uploads/2020/04/CRUSHCREATIVE_ICO_BRANDING_LOGO_NavyWhite-01-e1586189748878.pngThomas BIDAUX2013-09-03 10:55:092014-09-17 16:47:22Kickstarter UK – First half of 2013

Virtual Worlds Management has posted its update on

Virtual Worlds Management has posted its update on

{kind=link}